|

|

Letter to Adele Ferguson 5 Oct 2019 Defined Terms and Documents

3. In April 1985 the RBA

removed an 18% interest rate cap on Credit Cards when the Overnight Cash Rate was 17.2%.

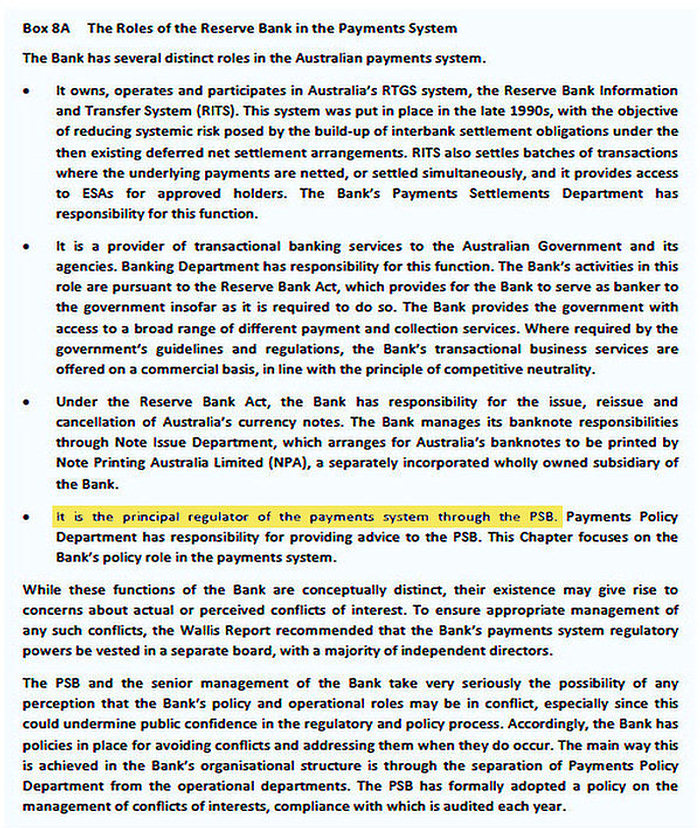

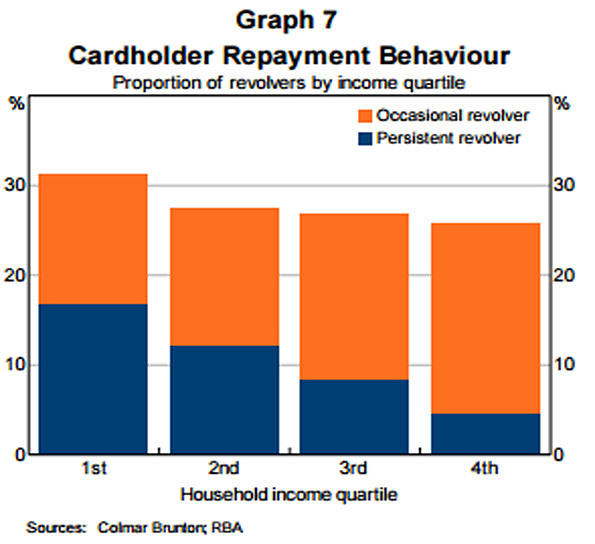

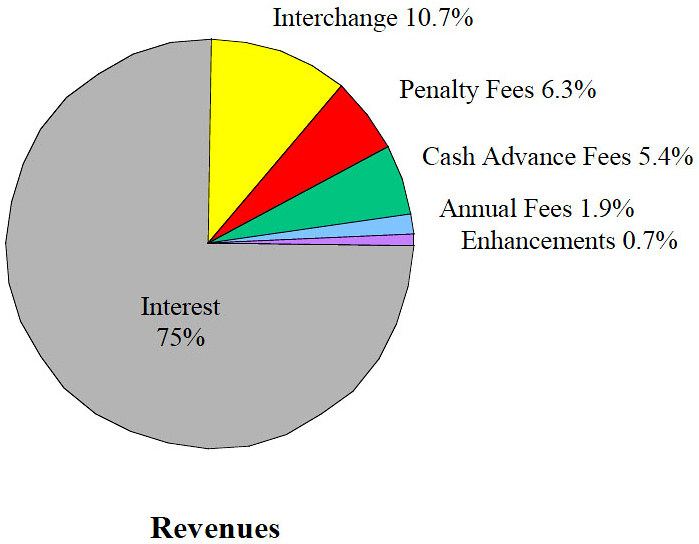

The RBA capped the maximum interest rate on Credit Cards in Australia at 18% until April 1985. The cap was withdrawn when the Overnight Cash Rate was a smidgeon over 17% during an era of very high inflation. Australia's Principal Regulator of the Payments System, the RBA, should have re-imposed a maximum interest rate on Credit Cards over 25 years ago when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16% - back in June 1992. Significantly, prior to the Campbell Report circa early 1980's, the RBA regulated all Australian bank interest rates with an Iron Fist - "... when de-regulation resulted in adverse consequences, re-regulation ensued...". Prior to The Campbell Committee recommendations Australian banks had been highly regulated - dating back to the failure of banks in the 19th century. The particulars of deregulation are well covered by: * "Overview of Financial Services Post-Deregulation - 2002 - Dr. Diana Beal * "CHANGES IN THE BEHAVIOUR OF BANKS AND THEIR IMPLICATIONS FOR FINANCIAL AGGREGATES - July 1989" - Battellino and McMillan * Consumer Affairs Victoria - Regulating the cost of credit - Research Paper No. 6 2006 * The Unpleasant Truth About Australian Banking - bankinfoline.com By its own admission in Box 8A of the Reserve Bank's Submission to the Financial System Inquiry - March 2014, "The Reserve Bank is the principal regulator of the payments system through the PSB." The payments system includes control over Credit Card Products. Persistent Revolvers, as identified by the RBA in Graph 7 'Cardholder repayment behaviour' invariably possess only Level 1 or Level 2 Financial Literacy Capacity (as measured by the Productivity Commission and the ABS). Persistent Revolvers have paid a horrible price since the 18% cap on Credit Card interest rates was removed by the RBA in April 1985 – Latitude Financial's Money Go MasterCard credit card had a Cash Advance interest rate of 29.49% until last March . It is now 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. There are over 16 million Credit Cards in Australia. Persistent Revolvers hold 12.58% of those 16 mil Credit Cards. Persistent Revolvers pay 80% circa of the Interest, Penalty Fees and Cash Advance Fees shown in the Credit Card Revenue pie chart. Chapter 5 and Chapter 17 note inter alia that between 1960 and 1980 the Reserve Bank diligently regulated Australian commercial bank interest rates relying on Section 50 of the Banking Act 1959 as amended. Until 1980 banks could not offer more than 3¾% on a passbook account and 6½% interest on a Savings Investment Account (minimum account balance of $500, deposits and withdrawals must be $100 or greater, and 7 days written notice had to be given to the bank for all withdrawals). "......... to achieve monetary policy, public sector financing and sectoral assistance objectives.....", as well as safeguarding against further bank collapses (chronicled in Chapter 17). Chapter 5 notes:

Prior to Aug 1993, Credit Card Issuers were restricted from charging an Annual Fee on Credit Cards as the various State Credit Acts prohibited most Credit Card Issuers from charging annual fees if they charged interest on credit card purchases (e.g. Credit Act 1984 (NSW) s 54). Following a recommendation from the Prices Surveillance Authority’s 1992 'Inquiry Into Credit Card Interest Rates', State legislatures issued exemption orders which allowed all financial institutions to charge both interest and fees on credit cards from 1 August 1993. Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed. "The tide of utilitarianism rose slowly, and a lengthy campaign was necessary before the financial deregulation of 1854, which abolished the British interest rate cap. However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War. We now trace the gradual lead-up to this second phase of regulation." "Obviously this is a pretty radical act, and it will be fought," he replied. "But I think the American people are disgusted with the financial industry. They want change. You could argue that an interest rate of 15% or 18% is more than enough to accommodate any amount of risk on the lender's part. If a loan appears riskier than that, don't make it. What we have to ask as a nation is whether it's ethical to charge people 30% interest rates," Sanders said. "This is loan sharking. Let's call it what it is." "the principal regulator of the payments system through the PSB", and Chair of the Council of Financial Regulators - (1) has extensive powers to, inter alia, request information from payment system participants and operators regarding Credit Cards under, amongst other clauses, Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998; (2) is bound to " ....inform the Government, from time to time, of the Bank's monetary and banking policy" under Section 11(1) of the Reserve Bank Act 1959 having regard to its obligations under Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 to "best contribute to.......... the economic prosperity and welfare of the people of Australia"; (3) holds authority under Division 4, Section 18 of the Payments System Regulation Act 1998 to set Standards that "are in the public interest" for a previously 'designated Payments System (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998 after having also imposed an Access Regime under Section 12. Re (2) above, sub clause (xiii) of Section 51 of the Australian Constitution behoves the Australian Parliament to place serious weight on any recommendation by the RBA re "banking". After sharing emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, Reserve Bank of Australia, the Writer posted his extensive submission (on 3 CDs and A4) to the RBA in Dec 2011 seeking application of the User Pays Principle. Section 8 of his submission accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001. "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." The RBA should then have imposed a maximum interest rate on all Credit Cards - 1. for all Purchases a maximum interest rate of 850 basis points; and 2. for all Cash Advances of 950 basis points, above the RBA official interest rate (Overnight Cash Rate). But it should have re-imposed a maximum interest rate over 25 years ago when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16% - back in June 1992. |

|

|

|

{kind=link}

{kind=link}

{kind=link}