Interest And Penalty Fees Revenue or Interest And Penalty Fees means Credit Card Issuers under Four-Party Schemes and Three-Party Schemes derive a material amount of their annual Interest And Fees Revenue from -

* Credit Cardholder Fees; and

The primary components of Credit Cardholder Fees are -

Interest Income is materially boosted due to the recent practice of Credit Card Issuers -

(A) charging Interest often at Usurious Unsecured Interest Rates on the entire Closing Balance for the previous month if the previous month's Purchases are unpaid by the Payment Due Date - even paid a day late or a dollar short; and

(B)

Withdrawing the

Interest Free Period on Purchases for up to the

subsequent two months - hence three months' interest is charged from the date of

each

Purchase

for up to three consecutive months

upon not paying the entire

Closing Balance

for the previous month by the

Payment Due Date as evidenced in

-

*

Example

1

-

Unconscionable

Conduct - St George Visa Card;

and

* Example 2 - Unconscionable Conduct - Coles 'No Annual Fee MasterCard' and Coles 'Rewards MasterCard'

The 80 - 20 Rule (Pareto Principle) applies to Credit Card Issuers' primary revenue source as 33% of Credit cardholders, known as revolvers, pay 100% of Interest And Penalty Fees Revenue.

12.58% circa of Cardholders identified by the Reserve Bank in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 - Submission 20 as Persistent Revolvers, that are Financially Uneducated And Vulnerable Australians, pay 80% circa of Interest And Penalty Fees. Put another way, 20% of Credit Cardholders pay 80% circa of Credit Card Issuers operating costs which includes a sizeable portion of the cost of Rewards Schemes that the Financially Educated enjoy a Free Ride - at no material cost and income tax free. Interchange Fees levied upon Merchants fund the remainder of Rewards Schemes.

The User Pays Principle which is applies in over 95% of the range/scope of financial transactions in Australia (eg. filling up the tank with petrol, going to the movies, buying a case of beer, paying the electricity bill, catching the bus to work, paying the rent or mortgage payment) is non-existent when enjoying a Line/s Of Credit with a Credit Card/s. As evidenced below, Net Interchange Fee income is immaterial to the P&L of a Credit Card Issuers.

|

|

|

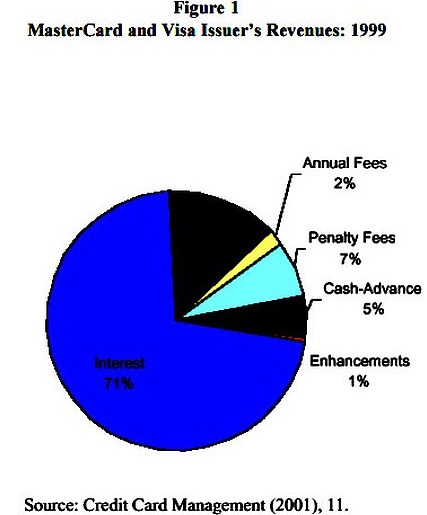

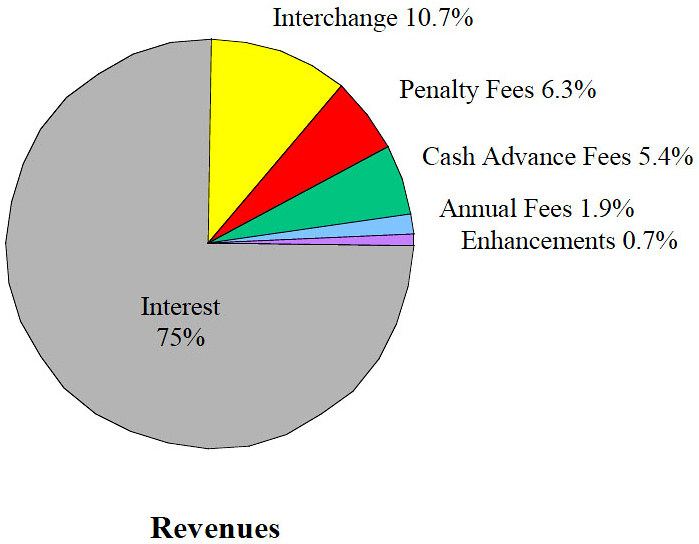

The above 'pie chart' (on RHS) appears in a journal report titled "Who Pays for Credit Cards?" dated 2001 which displays a break-up of Card Issuers' Revenues for the aggregate of Visa, MasterCard and Discover cards in the USA. It shows that net U.S. Interest Revenues of 75% and associated Penalty Fees Revenue (Late Payment Fees and Overlimit Fees) of 6.3% and Cash Advance Fees of 5.4% aggregate to 86.7% of U.S. Card Issuers' Annual Revenue. Interchange Fees charged to the Merchant are only 10.7%.

The following statement is from the Reserve Bank's Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015

So in Australia, where the RBA has materially pegged Interchange Fees (see quote immediately below), the percentage of Net Revenue from Interest and Late Payment Fees is likely to also exceed 80% of Total Net Revenues.

“What are the RBA's new interchange standards?

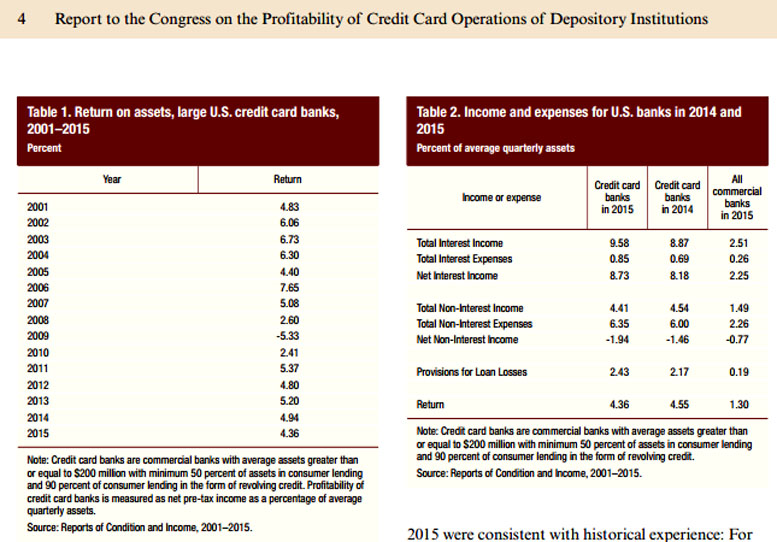

Significantly in the USA, the annual Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions - June 2016 includes the below Table 2 which shows that US Credit Card Issuers in 2015 had Net Interest Income of 8.73% and total non-Interest income of -1.94% of average quarterly assets.

2.9 While the RBA advised that about 75 to 80 per cent of credit card transactions do not accrue interest, about 65 per cent of the total quantum of credit card debt (or, as noted above, $33.1 billion) is accruing interest. To clarify, interest paying cardholders 'account for about 30–40 per cent of accounts, about 20–25 per cent of transactions, but close to two-thirds of the outstanding stock of debt'.9

10 Similarly, the CBA suggested the trend might be attributed to 'higher customer repayment rates and aggressive zero per cent balance transfer offers'.11