Order Of Payments means Balance Transfer Interest Free Period Offers (as summarised in Predatory Marketing) are an enticement to attract Credit Cardholders with high Outstanding Indebtedness over more than one Credit Card to seemingly gain respite from paying Usurious Unsecured Interest Rates by transferring their Outstanding Indebtedness to a different Credit Card Issuer which offers a 'Teaser Interest Rate' (sometimes 0%) for an 'Introductory Period' (from 3 months to 24 months) either with no one-off 'transfer fee' or a B.T. Amount fee up to say 3%.

History of Balance Transfers (by the disreputable CreditCards.com website) chronicles that Balance Transfer Interest-Free Period Offers first raised their ugly head in the USA in 1992 and entered the UK Credit Card market by the mid 1990s. Casual empiricism suggests that Balance Transfer Offers entered the Australian Credit Card Products by the late '90s.

Hidden discretely in Balance Transfer Offers was an 'Order of Payments' Allocation Practice in the fine print of the terms and conditions that specified which balance(s) the Credit Card Issuer of a Balance Transfer Credit Card would apply payments by the Credit Cardholder to firstly. In nearly all cases payments were applied to the lowest interest rate balances first and the highest interest rate last. Any payments by the Credit Cardholder were applied firstly to the Balance Transfer amount under a 'Teaser Interest Rate', whereupon any Purchases or Cash Advances were deemed unpaid and incurred interest at the specified interest rates from the date of each Purchase or Cash Advance. Hence, if you had a Balance Transfer amount, and you used the Balance Transfer Credit Card, you did not enjoy an Interest Free Period (referred to as a Grace Period in the USA).

Below is an extract from the Woolworths Everyday Money MasterCard Credit Card pre 1 July 2012:

The Guardian article "Interest-free credit card trap snaring unwitting borrowers" - 25 March 2012 notes, 'inter alia' that:.

"Brian Cole, of Capital One in the UK, the bank that first introduced zero-interest balance transfers to Britain in the 90s, says: "There's a lot of practice in the [banking] marketplace that is shameful, and credit card companies are not immune. [Balance transfer] customers think they're going to progress in getting out of debt, and get some relief from interest payments. But make a mistake and you will end up making money for your credit card company."

Alas some Credit Card Issuers devised new methods to exploit Australian Credit Cardholders s with poor Financial Literacy as exampled in Labyrinth of ‘Concealed Spiders’:

(A) Example 3 highlights that some Credit Card Issuers of Balance Transfer Credit Cards have since introduced, but not overtly publicised to prospective new customers, that an Interest Free Period will not apply on Purchases until after the Balance Transfer amount is repaid in full and the Credit Cardholder has repaid its Total Amount Owing, including its Balance Transfer amount.

(B) Example 4 highlights that on some of the Balance Transfer Interest-Free Period Offers, should the Credit Cardholder make a Purchase/s and not repay their Balance Transfer amount and any Purchase/s by the Payment Due Date, s/he will not only be charged interest on the aggregate of their Purchases and the Balance Transfer amount, but also forego their Interest Free Period for the subsequent two months.

(C) Some Credit Card Issuers of Balance Transfer Credit Cards provide a Calculator for prospective new customers to determine how much interest they could save during the 'Teaser Interest Rate' (sometimes 0%) for an 'Introductory Period' (from 3 months to 24 months). Hidden in the fine print is An assumptions that this calculator makes is that "You don’t make any purchases on your card until the promotional period ends or the balance transfer is paid in full." See Calculate how much interest you could save!

Re Example 1 in Labyrinth of ‘Concealed Spiders’, below is an extract from the St George Bank Vertigo Platinum Card webpage:

However, it may be gleaned from the Writer's on-line 'Chat' with Stavroula at St George Bank on 13 Jan '15 that St George offers an Interest Free Period of 3 months on Purchases, in addition to an Interest Free Period on the Balance Transfer amount to approved customers. However, after that initial 3 months, St George charges interest @ 12.74% p.a. on Purchases for 3 months after any Balance Transfer amount is repaid.

Stavroula: After 3 months, if your closing balance is paid in full you can take advantage of the up to 55 day interest free period by consecutively paying your closing balance in full by the statement due date for the next 2 statements at least.

By maintaining a discipline of not making Purchases or not making any Cash Advances altogether, a Credit Cardholder can ensure it maintains the full benefits of the original Balance Transfer Interest-Free Period. However, few Credit Cardholders which switch their Outstanding Indebtedness from their Credit Card to a (new) Balance Transfer Interest Free Period Credit Card are unaware of the perils of making a Purchase/s. Some others that are aware exhibit requisite discipline, more likely when assisted by a 'Financial Counsellor', that works for one of 44 Australian charities which Australian Governments fund approx. $11 million annually.

Because transferring to new credit cards often results in lowered rates, one could seek to repeatedly make use of this process to save quite a lot of money over the years. The idea is to switch to a new low Balance Transfer Credit Card the moment the previous Balance Transfer 'Teaser Interest Rate' has expired. However, a caveat as the Credit Card contract might include a clause preventing the Credit Cardholder from transferring the balance a second time within a certain period of time.

To deter Credit Cardholders switching to another Credit Card Issuers' Balance Transfer Interest-Free Period Credit Card, some Credit Card Issuers' of Balance Transfer Interest-Free Period charged a Balance Transfer Fee. Citibank is offering 0% p.a. for 24 months on balance transfers. A 3% Balance Transfer Fee applies. Hence, if the Balance Transfer amount is $2,000, the Balance Transfer Fee is $60.

Most Credit Card Issuers do not charge any interest for up to 24 months on the Balance Transfer amount because the -

(a) RBA's Cash Rate to buy large 'parcels' of cash is only 1.5%; and

(b) Cash Advance interest rates often around 22%. are Usurious Personal Loan Interest Rates -

* once the 'Introductory Period' has expired; or

* more likely once monthly repayments have wiped out the 'Balance Transfer Amount' - as explained in the second para above.

The highest Cash Advance interest rate is 29.49% from G.E. Money's "Go MasterCard"

The National Consumer Credit Protection Amendment (Home Loans and Credit Cards) Bill was passed on 4 July 2011 and was enacted as at 1 July 2012, whereupon Credit Card Issuers were no longer able to apply the afore-mentioned 'Order of Payments' Allocation Practice, but must now apply a Credit Cardholder's payment/s to the highest interest rate debt, namely the most expensive part of a Credit Cardholder's Credit Card Outstanding Indebtedness.

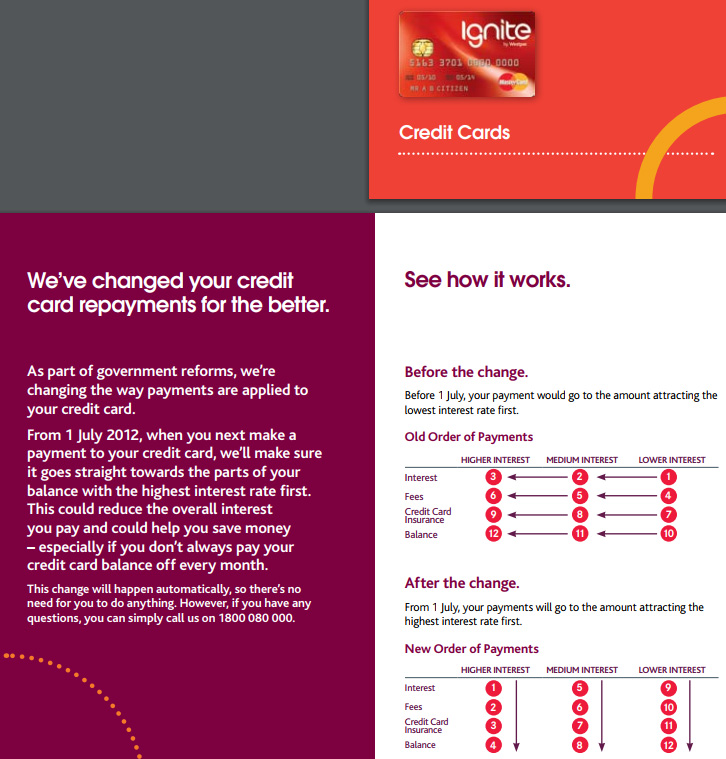

Above is a

Print Screen of page 3 of Westpac's document 'Changes to your

credit card payments' which shows that -

*

prior to

1 July 2012, payments were applied to the lowest interest rate first; and

*

from 1

July 2012, payments were applied to the highest interest rate first.

See:

The interest-free credit card trap snaring unwitting borrowers - The Guardian - 25 March 2012

What You Must Know Before Transferring Credit Card Balances

Zero-interest balance

transfers credit cards can have sting

'Zero balance' credit card deals under ASIC microscope

How to effectively use a "Balance Transfer":

finder.com.au provides "Find out about the Credit Card Reforms happening 1st July 2012".

Balance Transfer Credit Cards - finder.com.au - 11 Sept 2017