As detailed in the Writer's

Submission to Maurice Blackburn

dated 25 June 2017

seeking a

Class Action

against the RBA for breach of

its

Statutory Duty

and

Fiduciary Duty,

400,000

circa

Credit Cardholders across Australia

-

a)

have paid in excess of $20,000 each in

Interest and Penalty Fees

(charged at

Usurious

Interest Rates) during up to a continuous

nine years period at an average

Comparison Rate Over

18% Per Annum;

b)

were misled by

Predatory

Advertising

Targeted At Credit Cardholders With Low

Financial Literacy

Capacity that

constitutes

Unconscionable Conduct;

c)

have suffered

Extreme Financial And Emotional Distress;

and

d) posses poor

Financial Literacy Capacity

(predominantly Level 1 or below, and some Level

2) as -

(i) identified and quantified by the Productivity Commission,

the ABS and ASIC separate written reports (Chapter

1); and

(ii) evidenced on a daily basis by 500

circa

Financial Counsellors

employed by 44

charities/community organisations that collectively receive $43 million annually

from the Commonwealth Govt. ($20m) and the State Govts ($23m) via

Financial Counselling Australia

(Chapter 7).

Hardly a month goes by without another

newspaper article,

or report by

ASIC,

the

Reserve Bank

or a plea from a

Credit Card Distress Authority,

regarding the debt burden born by a small number of

Credit Cardholders, invariably with

Poor Numeracy and Literacy

Skills

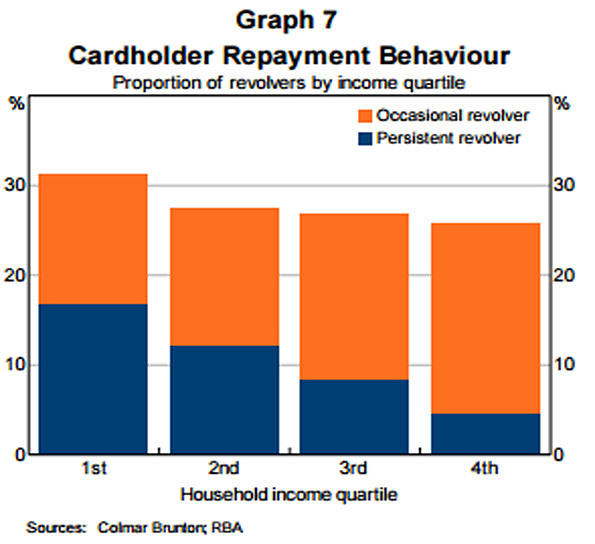

that the RBA has referred to as

Persistent Revolvers. Meanwhile

two thirds of Credit Cardholders, described by the RBA as

Transactors, enjoy their

Lines of Credit a virtually no

cost, because

Annual

Cardholder Fees account for only 2% of

Interest And Penalty Fees Revenue.

Is Australia really an egalitarian country?

Five

Prime Ministers have talked it, but our Federal Govt hasn't walked it,

obligated under

Section 51 (xiii) of the Australian Constitution, to

the detriment of

Financially Uneducated And Vulnerable Australians

that possess, through no fault of their own, poor

Financial Literacy Skills;

some Credit Card Issuers have deployed

Predatory Advertising and

charged Usurious Interest Rates

and Penalty Fees, Targeted At Credit Cardholders With Low

Financial Literacy

Capacity.

St Vincent de Paul, Salvos, Anglicare et al provide a welter of

Financial

Counsellors where

Credit Card Debt

Accruing Interest, often spread over several

Credit Cards, is invariably the root of

Extreme Financial And Emotional Distress.

Australian Governments

allocate $43.38 million annually to 44 Australian charities to provide

financial counselling to Australians that are experiencing

Extreme Financial And Emotional Distress.

National Debt Helpline is a not-for-profit service that provides

professional counsellors to help Australians tackle their debt problems.

{kind=link}