Below is an extract from

RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015 - Submission 20 - Senate Economics References Committee - Introduction"The Cost of Credit Cards to Merchants

As recognised by the Terms of Reference, interchange payments (and the loyalty programs they finance) increase the costs of payments for merchants and accordingly drive up the final prices of goods and services for all consumers, including for consumers who do not use credit cards.

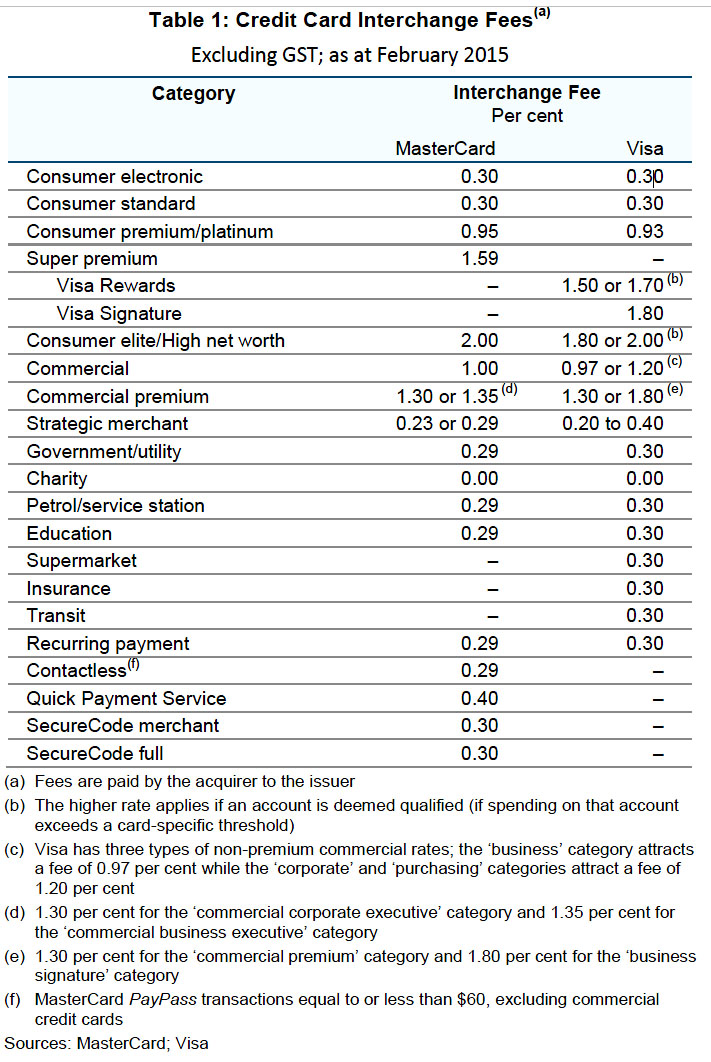

The interchange schedules for the MasterCard and Visa credit card systems include a wide range of interchange rates from 0.20 per cent or 0.23 per cent for some ‘strategic’ large merchants to 2 per cent for the highest level of premium cards (Table 1). Based on the hierarchy of interchange rates, the cost of the high interchange rates on premium or commercial cards falls entirely on small merchants and other merchants that do not benefit from special rates.

There are two significant consequences of the current structure of interchange schedules. First, there are now large differences in the average interchange rates paid on the transactions of strategic or qualifying merchants compared with other merchants. The Bank estimates that the average credit card interchange rate for non-preferred merchants (i.e. those not benefiting from strategic or other preferential rates) was more than 50 basis points higher than the interchange rate applying to preferred merchants in the December quarter of 2014. These differences in interchange rates have a corresponding effect on the merchant service fees faced by the two groups which is in addition to the

higher margin that acquiring banks would normally apply to small merchants relative to large merchants. The second consequence of the complex interchange fee schedules is that the non-preferred merchants have little transparency over the cost of particular transactions. In the case of a MasterCard or Visa credit card transaction, the interchange rate will be 30 basis points on a standard card but will be 200 basis points if the transaction involves the highest level of premium card. In contrast, for strategic merchants the cost of all cards issued in Australia, from standard non-rewards cards to the highest level of premium cards, will be constant (and as low as 0.20 per cent).

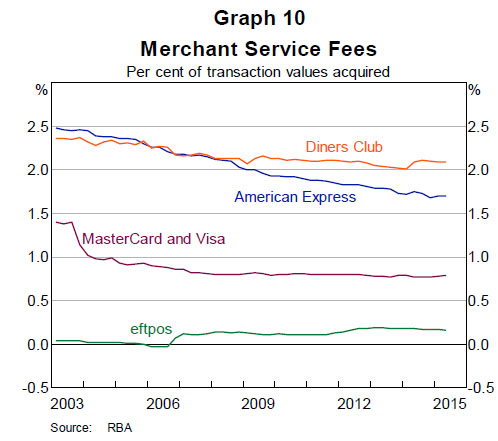

The Bank (RBA) collects data on average merchant service fees for the different payment schemes (Graph 10). For the June quarter 2015, merchant service fees were around 2.1 per cent for Diners Club, 1.7 per cent for American Express, and 0.79 per cent for MasterCard and Visa, though the latter also includes debit card merchant service fees. The Bank estimates that merchant service fees for MasterCard and Visa credit cards were around 0.87 per cent in the June quarter.

Merchants have some ability to recoup the costs of more expensive payment methods via the use of surcharging for such payments. While the majority of merchants do not surcharge for particular payment methods, the right to surcharge is important to promote efficiency in the payments system and is also a means by which merchants can exert some downward pressure on the cost of payments. There are, however, some instances of firms in particular industries which may be surcharging excessively for some customers; the Bank is currently consulting on this issue as part of its review of the regulatory framework for cards payments."

See:

Credit Risk To Credit Card Issuers

Cost of Credit Card transactions to Cardholders

Interest rates on credit card debt