Cost of Credit Card Transactions to Cardholders

Below is an extract from

RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015 - Submission 20 - Senate Economics References Committee - Introduction"The cost of credit card transactions to cardholders

The Payment Costs Study also provides data on the cost of credit cards and other payment methods to end-users. In the case of consumers, it is useful to distinguish between the average cost of a payment method and the marginal cost for a particular transaction. In addition, it is important to consider the net cost to consumers – that is the costs they pay less any financial benefits they receive in the transaction.6

Estimates from the Payment Costs Study suggest that the average net cost to consumers of MasterCard and Visa credit cards was around 19 cents per transaction, where this includes the costs and financial benefits associated with the payments function but not any subsequent interest payments. This compares with costs of around 21 cents for debit card transactions and 13 cents for cash transactions. That is, the net cost to consumers of credit card transactions was around the same as for debit cards and only a little above that for cash, despite the considerably higher overall resource cost of credit cards compared to these other methods. To hold a credit card, consumers typically pay annual and other fees; on average, these fees are equal to around $0.84 per transaction. At the time of the transaction, consumers receive a sizeable inward transfer from financial institutions equivalent to around $0.77 to use the credit card due to the interest-free period and reward points available on credit card transactions. Consumers may also pay a merchant surcharge at the point of sale (of around $0.12 per transaction on average). In terms of incentives at the time of a transaction, the existence of the interest-free period and reward programs means that consumers face a significant incentive to use credit cards over other payment methods.

6 The incentives discussed here ignore some of the potential benefits for credit card holders and consumers of different payment methods. For example, card payments may provide consumers with the benefit of a greater feeling of security as they reduce the need to carry large cash holdings; on the other hand, some consumers report in surveys that they prefer the budgeting discipline that cash or debit cards bring relative to credit cards.

The rewards programs offered by credit card issuers are due in large part to the existence of interchange fees that are paid by the card acquirer (the merchant’s financial institution) to the issuer (the cardholder’s bank) in each transaction in four-party card schemes (see Box B). These are then passed on to merchants by acquirers in the form of a higher merchant service fees. In the case of three-party card schemes (such as American Express or Diners Club) there is no direct equivalent to interchange fees, with rewards programs funded directly from merchant service fees charged by the card scheme.

The interchange fee payable on a four-party card transaction depends on the category of that transaction within a schedule of interchange rates set by the scheme. The average level of interchange rates is subject to a Reserve Bank standard that requires that the weighted average of the schedule of rates does not exceed 50 basis points, with compliance required once every three years (or at the time of any reset of the schedule). The specific rate applying to a transaction will depend on the type of merchant (‘strategic’, service station, etc), the type of card (various types of premium cards, corporate, etc) and the nature of the authentication (contactless, SecureCode, etc) or the value of the transaction. There is a hierarchy of categories, which determines how the merchant, card and transaction categories interact. Typically, the relatively low ‘strategic’ interchange rates for large merchants have precedence over the interchange category for the type of card, so that the same relatively low rate for strategic merchants applies for all their transactions, including for those transactions using premium cards with high interchange rates. However, merchants that do not have access to strategic or merchant-specific rates will face different rates based on the type of card presented.

In recent years, there has been significant growth in the premium segment of the credit card market, with the emergence of ‘super-premium’ and, more recently ‘elite’/‘high net worth’ credit cards in addition to ‘gold’ and ‘platinum’ cards. Issuing banks can earn higher interchange fee revenue on these products than from standard credit cards, and may use this revenue to fund more generous rewards programs in terms of frequent flyer points, spending vouchers at retailers, travel insurance, etc. One objective measure of the generosity of rewards to consumers is in terms of the card spending required to generate a $100 voucher, which can be translated into an effective cash-back percentage. Data on the interchange rates and rewards on offer in a sample of around 80 cards monitored by the Bank, show a positive correlation between the interchange rate on cards and the generosity of rewards by issuers (Graph 9).

|

Box B Interchange Fees

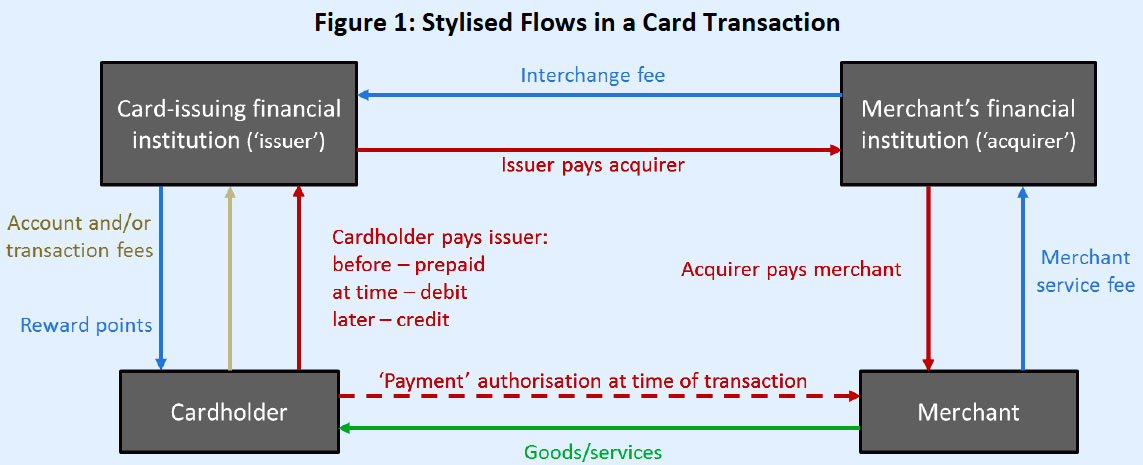

An interchange fee is a fee charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. They are most commonly seen in card transactions, although can arise in other payment methods.7 A typical card transaction (Figure 1) involves four parties – the cardholder, the cardholder’s financial institution (the issuer), the merchant and the merchant’s financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer. Interchange fees can have important implications for the prevalence and acceptance of different cards as well as the relative costs faced by consumers and merchants. In contrast to normal markets for goods and services, competition in payment card networks can actually drive fees higher.

Financial institutions typically charge fees to their customers for payment services. Cardholders are charged by their financial institution in a variety of ways. In the case of payments from a deposit account such as debit cards, financial institutions typically charge a monthly account-keeping fee and, sometimes, a fee per transaction (or for transactions above a certain number). In the case of payments using a credit card, financial institutions usually charge an annual fee rather than a per transaction fee, and interest is charged on borrowings that are not repaid by a specified due date. Merchants receiving payments are also typically charged by their financial institutions. The fees paid by merchants usually depend on the payment method. For credit and debit cards, merchants are usually charged a ‘merchant service fee’ for every card payment they accept. Some merchants are also charged a fee by their financial institution to rent a terminal to accept cards. In contrast, interchange fees are paid between financial institutions and are present in many, but not all, card systems.8 Interchange fees are often not transparent; cardholders and merchants do not typically see them. But they have an impact on the fees that cardholders and merchants pay. In the MasterCard and Visa credit card schemes, interchange fees are paid by the merchant’s financial institution to the cardholder’s financial institution every time a payment is made using a MasterCard or Visa card. This has two effects. First, the merchant’s financial institution will charge the merchant for the cost of providing it with the acceptance service plus the fee that it must pay to the card issuer (the interchange fee). The higher the interchange fee that the merchant’s financial institution must pay, the more the merchant will have to pay to accept a card payment. Second, since the card issuer is receiving a fee from the merchant’s financial institution every time its card is used, it does not need to charge its customer – the cardholder – as much. The higher the interchange fee, therefore, the less the cardholder has to pay. In effect, the merchant is meeting some of the card issuer’s costs which can then be used to subsidise the cardholder. Indeed, with rewards programs, the cardholder may actually be paid to use his/her card for transactions. Where the market structure is such that there are two payment networks whose cards are accepted very widely (i.e. merchants accept cards from both networks), and where consumers may hold one network’s card but not necessarily both, competition tends to involve offering incentives for a consumer to hold and use a particular network’s cards (loyalty or rewards programs, typically). A network that increases the interchange fee paid by the merchant’s bank to the cardholder’s bank enables the cardholder’s bank to pay more generous incentives, and can increase use of its cards. However, the competitive response from the other network is to increase the interchange rates applicable to its cards. In the early 2000s, the Reserve Bank became concerned that credit card holders were effectively being subsidised to use their credit cards through arrangements that added to merchants’ costs. Interchange fee revenue allowed card issuers to support generous credit card rewards programs and, as a result, many credit card holders were facing a negative effective price for credit card transactions, even though those cards had positive costs for the system as a whole. This distorted price signals to cardholders about the relative costs of using different payment instruments. The Reserve Bank therefore introduced a number of reforms to the credit card market from 2003, with the aim of improving efficiency and competition in the Australian card payments system. Among other things, the reforms reduced interchange fees, which had been used by card issuers to support attractive rewards programs on credit card products. Overall, reward points and other benefits earned from spending on credit cards have become less generous, although card schemes have found ways, within the bounds of the Reserve Bank’s regulation, to increase incentives for card issuers to promote particular products within their suite of offerings. Over time, MasterCard and Visa have progressively introduced new, higher fee categories for consumer and business cardholders, based on the type of card held (e.g. premium/platinum, super premium, ‘elite’/‘high net worth’). This enables issuers to pay more generous incentives to holders of these cards; card issuers have responded, particularly through new strategies focusing on the premium segment of the market. |

7 There is now a substantial theoretical literature on the role of interchange fees in card systems; see Verdier (2011) for a recent survey.

8 For example, the European Commission (2013) notes (p 53) that ‘in Norway, the absence of IFs [interchange fees] for debit cards is accompanied by very high level of card acceptance by merchants and usage. Denmark also has one of the highest card usage rates in the EU at 216 transactions per capita with a zero-MIF [multilateral interchange fee] debit scheme. This is also true of international schemes: in Switzerland Maestro has no MIF and is the main debit card system. It is also worth noting that all European card schemes were originally created without MIFs. MIFs have been introduced by banks and card schemes only later.’

See:

Credit Risk To Credit Card Issuers

Cost of Credit Cards to Merchants

Interest rates on credit card debt