Interest rates on Credit Card debt

Below is an extract from

RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015 - Submission 20 - Senate Economics References Committee - Introduction"Interest rates on credit card debt

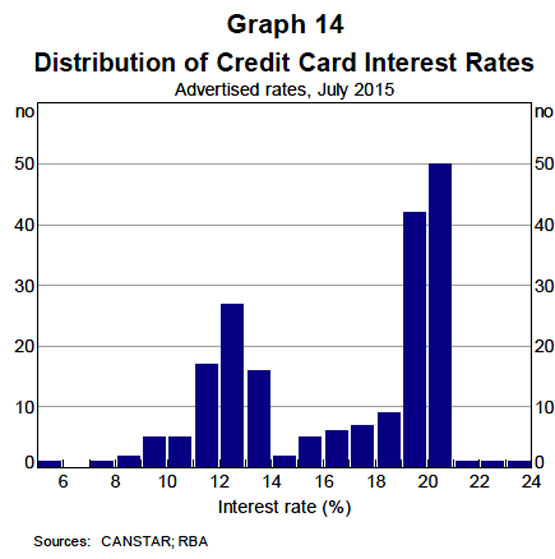

There is significant variation in the advertised rates on credit card debt, reflecting the wide range of products offered, but some bunching of standard cards around 20 per cent and around 13 per cent for lower-rate cards (Graph 14).

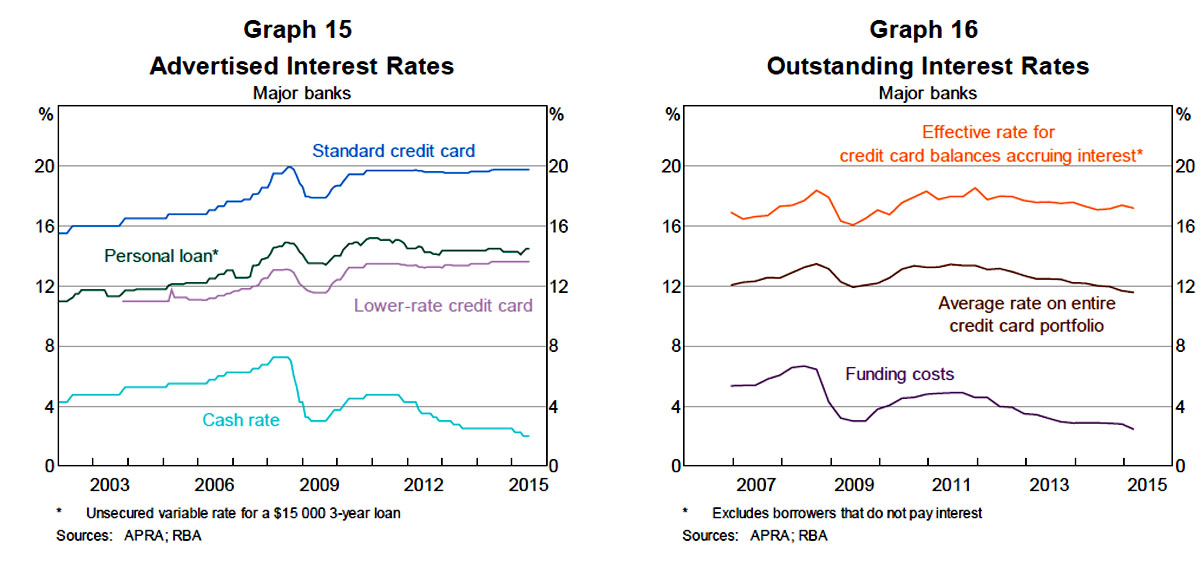

The Bank publishes data on average advertised credit card interest rates for ‘standard’ and ‘low-rate’ cards. Since around 2010 the average interest rate for standard cards has been fairly steady at just under 20 per cent, while for lower-rate cards the average interest rate has been about 13 per cent (Graph 15). These data are average advertised (ongoing) interest rates rather than the average interest rate actually paid by all holders of standard or lower-rate cards. For instance, the relatively stable advertised rates in recent years do not take into account low- or zero-rate balance transfer offers that cardholders may receive for switching their outstanding credit card debt to another bank.

Consequently, average interest rates paid may be lower than the advertised ongoing rates, to the extent that cardholders have been switching banks to take advantage of these deals. More generally, the advertised interest rate on a card is only relevant to those cardholders who do not pay off their monthly statement in full and have a stock of outstanding debt.

Data collected by APRA from the major banks provide some further information on actual interest rates on their credit card portfolios (Graph 16). These data indicate that the actual average interest rate on the entire book of credit card loans (including debt that does not yield interest) was 11.6 per cent in the March quarter. While advertised credit card rates have been little changed in the recent period, the effective interest rate received by banks on their entire credit card portfolio has fallen by close to 2 percentage points since mid 2011. The effective interest rate on the entire credit card portfolio does not, however, provide a guide to the experience of those cardholders who pay interest on their credit card debt. Based on data reported reported to the Bank showing that around 35 per cent of outstanding credit card debt did not bear interest, the effective average interest rate for those borrowers that pay interest is estimated at about 17 per cent, down about 1 percentage point from 2011. Taken together, the recent changes in these two series are consistent with the observed decline in the proportion of the stock of debt that is accruing interest (either reflecting more consumers paying down debt ahead of being charged interest, or reflecting an increase in the take up of zero-and lower-rate balance transfers) and also some switching by consumers from high- to lower-rate cards. The major card-issuing banks would be able to shed further light on these estimates.

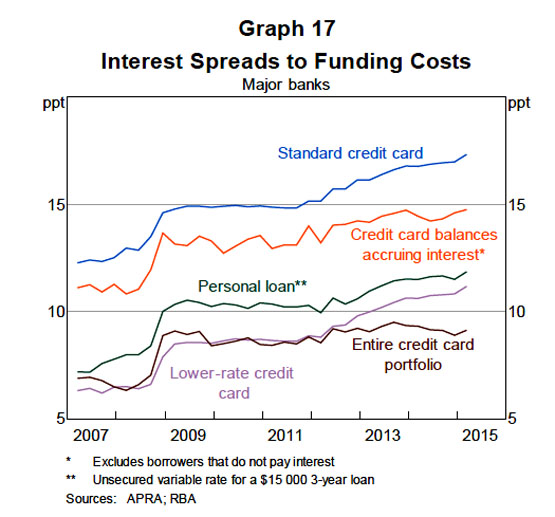

Based on estimates of the overall cost of funds for banks, it is possible to calculate the spreads on different lending rates (Graph 17).

11 The data indicate that the interest rate on bank credit card portfolios is around 9 percentage points above the cost of funds, while the spread for those borrowers who are paying interest is about 14¾ percentage points. These spreads rose significantly in the global financial crisis (when funding rates fell significantly but credit card rates fell by much less) and have remained at that level or drifted modestly higher since.

The observation that issuers compete actively for customers yet credit card interest rates are high and do not closely follow changes in funding costs is consistent with international experience and has been studied by academics. The most well-known paper addressing this issue is a study by Ausubel (1991) for the United States. The study notes the apparent paradox that a market with few barriers to entry and the presence of 4 000 competitors could be characterised by very sticky interest rates and card issuers making much higher rates of return on their credit card lending than on other lines of business. Based on the work of Ausubel and others, it seems reasonable to explain the apparent paradox as resulting to a large extent from the existence of a significant number of consumers who are either not well informed or (for various behavioural reasons) are reluctant to switch banks or seek a lower rate. At the same time, banks may have little incentive to lower interest rates, given that rates are not a determining factor for many individuals who may (possibly mistakenly) not expect to build up significant balances, while in the case of other individuals, banks may worry that lower rates may attract lower-quality borrowers."

See:

Cost of Credit Card transactions to Cardholders

Credit Risk To Credit Card Issuers

Cost of Credit Cards to Merchants