Below is an extract from RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015 - Submission 20 - Senate Economics References Committee - Introduction

"Credit Risk To Banks

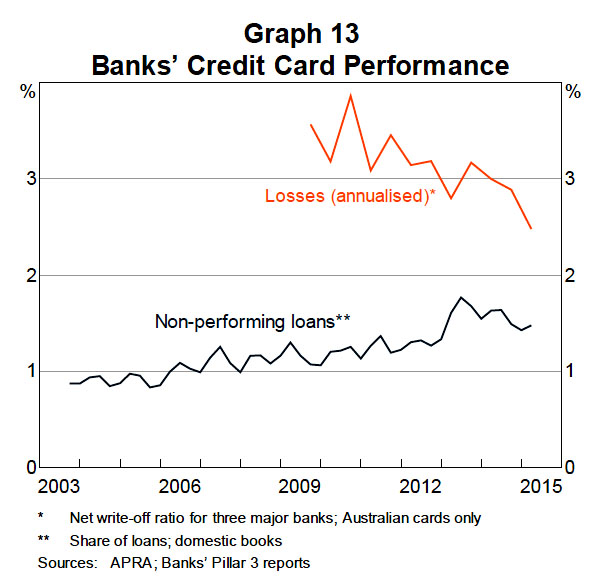

There is relatively limited information available on the risk of credit card lending. Data reported to APRA indicate that the non-performing loan (NPL) rate on banks’ credit card debt (defined as where repayment is more than 90 days past due or otherwise doubtful) has increased gradually during the past decade, although it has declined slightly over the past couple of years. The credit card NPL rate stood at 1.5 per cent as of early 2015, which is lower than the comparable ratio for other personal loans.

However, the overall loss rate for credit card issuers is probably higher than suggested by the NPL rate. Unlike some other types of household loans such as residential mortgages, credit card loans are unsecured, with little prospect, in some cases, of recovering a significant portion of the debt if the borrower defaults. As a consequence, some credit card debt may be written-off directly to an issuing institution’s profit and loss account, without first being recorded as a non-performing loan.

Data from the financial statements of three major banks suggest that the overall loss rate on their credit cards has been falling over the relatively short five-year period for which the data are available, and stood at 2.5 per cent as of early 2015 (Graph 13).10 This loss rate represents an average calculated over all users of credit cards; it is reasonable to assume that banks’ risk models expect lower loss rates for some account holders and higher rates for others, for example borrowers who have tended to be revolvers."

See:

Cost of Credit Card transactions to Cardholders