|

Defined Terms and Documents

Example 5 -

Unconscionable Conduct -

ANZ's 'First Visa Card' and 'Low Interest Visa Card'

ANZ's advertising of its 'First Card' and 'Low Interest Card' seeks to mislead

prospective new

Cardholders, particularly

Financially Uneducated And Vulnerable Australians,

that if they pay their

'Closing Balance'

as defined on page 65 of its 98 pages

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS"

that

any prospective new 'First Visa Card'

or 'Low Interest Visa Card'

Cardholder would

enjoy "Up

to 44 days interest free on purchases3. as asserted in

its webpage at 'Features and benefits'. But that is

not the case.

ANZ

has breached its obligations under

Regulation 28LFA

of the

National Consumer Credit

Protection Amendment

(Home Loans and Credit

Cards) Act 2011 due

to a legal drafting error in its definition of

Closing Balance which does not

include

Balance Transfer amount;

this omission has

resulted in ANZ charging vast amounts of interest at 19.74% p.a. on its 'First Card' and

'Low Rate Card' @

13.49% p.a. beyond the terms of its definition of

Closing Balance.

ANZ's offer letter and attachments (5 pgs of offer documents) -

I.

"0% p.a. first 16 months

on balance transfers"

offer letter to Ms. K. G_rd_n dated 5 Jan '15 [1 pg] lists

"how much you could save"

over 16 months by transferring an existing credit card debt

balance (eg $5,000 debt balance could save $1,251 in interest, $8,000 debt

balance could save $2,001 in interest), with the interest rate on Purchases for the

"First Card" 19.74% and "Low Rate Card" 13.49%;

II.

'Choose the ANZ credit card that

is right for you'

[1 pg] lists 'inter alia' that in order to enjoy

"Interest Free Days on Purchases"

you had to comply with the below 'fine print' clause 4:

4. Interest free periods on the purchases do not apply if you do

not pay your Closing Balance (or, if applicable, your 'Closing

Balance' less Instalment Plan and Buy Now Pay later plan

balances) shown on each statement of account in full by the

applicable

Due Date. Payments to your account are applied in the

order set out in the

ANZ Credit Cards Conditions of Use;

III.

'Key facts about this credit card'

[1 pg] notes 'inter alia'

adjacent to

'Interest-free period':

*

"up to 44 days on

the purchase balance" for the ANZ First Card

*

"up to 55 days on the purchase balance"

for

the ANZ Low Rate Card;

IV.

'Credit Card Application Form'

[2 pgs]

provides a paper based application form for the ANZ First Card or the ANZ Low

Fee Card.

ANZ's

afore-mentioned offer documents (posted to the Writer's home

address) which aggregate to 5 pages do not explain

that -

A. the only

way to achieve the material savings of $2,001 in interest costs on an $8,000

existing debt Balance Transfer is to

not make any Purchase/s during the initial 16 months; making

a

Purchase/s is the fundamental

purpose of holding a Credit Card. If any

Purchase/s is made whilst ever any part of the

Balance Transfer amount @ 0% interest for 16 months remains unpaid, then interest is charged (at the below

interest rates) from the date

of each Purchase (with no

Interest Free Period entitlement):

* "First Card" @

19.74% p.a.

* "Low Rate Card"

@ 13.49% p.a; and

B "If

you don't pay the full Closing Balance shown on a statement of account by the

applicable Due Date, the purchases balance will attract interest. However, you

may regain the benefit of interest free periods on purchases by paying the full

Closing Balance shown on two subsequent consecutive statements by each

applicable Due Date."

- refer

FAQs

How does the interest free period work?

Hence, if a

Cardholder makes any

Purchase/s and does not repay

the

Balance Transfer amount 'in toto',

then he/she pays interest on a "First Card" @

19.74% p.a. on all Purchases during that month from the date of each

Purchase.

In addition,

s/he forfeits

the

Interest Free Period for the subsequent two months, whereupon

a

"First Card" Cardholder continues to

pay interest at the

Usurious Interest Rate

of 19.74% p.a.

for an additional two months until his/her

Interest Free Period is re-installed - a

total of three months interest on all

Purchases @ 19.74%

p.a. (The RBA's official Cash

Rate is 2.25% p.a. as at 1 May '15)

Further below is a 'screen print' of ANZ's webpages for its

First Visa Card.

ANZ recognizes (on

page 10 of its 98 pages booklet titled

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS")

that it has misled many new Cardholders, which includes

its

First Visa Card Low annual fee $30, into believing that they

would enjoy, with regard to the

First Visa Card, "Up

to 44 interest free days on purchases3"

when, in fact,

First Visa Cardholders are charged at the

Purchase interest rate of

19.74% pa from the date of each

Purchase. This acknowledgement of a

misconception

by ANZ is

reprinted in yellow

background immediately below

and evidenced in detail in this webpage:

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account.

Whilst

interest

will

not

be

charged

on

the

0% balance

transfer,

interest

will

still

be

charged

in the

normal

manner

on

any

other

debits

to your

account. For

example,

interest

will

be

charged

on

your

purchases

balance,

except

to the

extent

an interest

free

period

applies."

The

amount of the

0%

balance

transfer

will

be included

in the

Closing

Balance

shown

on

a relevant

statement

of

account. Accordingly, an interest

free

period

will

generally

not

apply

in relation

to relevant

purchases

if

you

do

not

pay

the

full

Closing

Balance

(including

the

0%

balance transfer)

for

such

a

statement

of account

by the applicable

DUE

DATE.

In the above

extract from page 10 of ANZ's

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS" ANZ

acknowledges that many new

Cardholders that enjoy a

Balance Transfer

misconceive/misunderstand and wrongly believe that, in the case of the

First Visa Card Low annual fee $30,

that they enjoy "Up

to 44 days interest free on purchases3."

as asserted in its webpage at 'Features and benefits' below.

Below is clause 3 under 'Important information' from the below ANZ First

Card webpage:

3.

Interest free periods on the purchases do not apply if you do

not pay your Closing Balance (or, if applicable, your 'Closing

Balance' less Instalment Plan and Buy Now Pay later plan

balances) shown on each statement of account in full by the

applicable

Due Date. Payments to your account are applied in the

order set out in the

ANZ Credit Cards Conditions of Use.

ANZ has commenced the words

Closing Balance

with a capital letter which

constitutes a 'defined term' or 'definition'.

ANZ has not provided a definition of

Closing Balance

in its below

extracted webpage advertising its

First Visa Card Low annual fee $30.

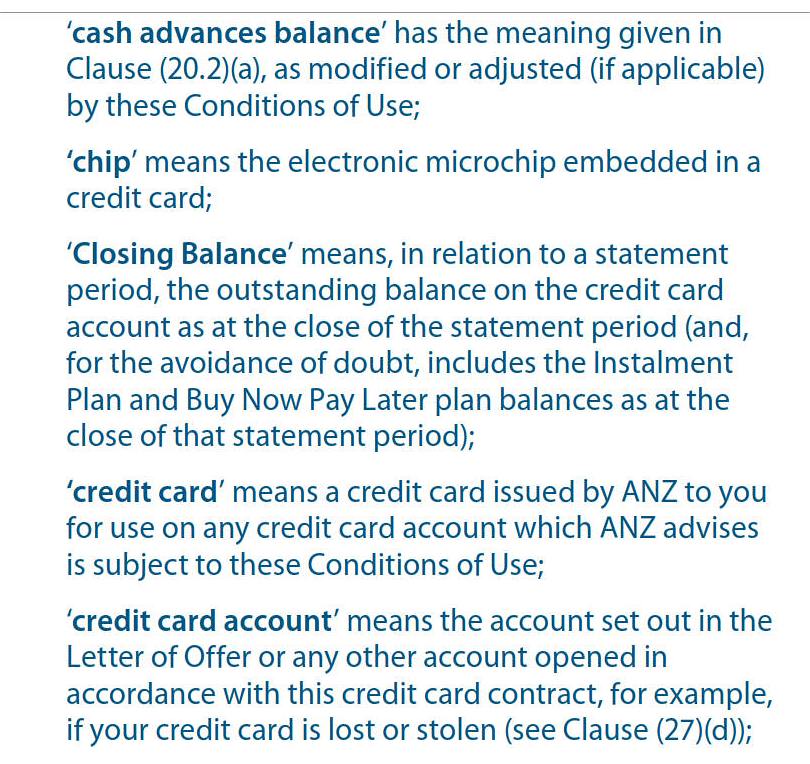

ANZ provides the below definition of 'Closing Balance' on page 65

of its 98 pages

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS". (Page 65 commences 48

'Definitions' under heading 'Meaning of words'):

‘Closing

Balance’

means,

in

relation

to a

statement

period,

the

outstanding

balance

on the

credit

card

account

as at the

close

of

the

statement

period

(and,

for the

avoidance

of

doubt,

includes

the

Instalment

Plan

and

Buy

Now

Pay

Later

plan

balances

as at the

close

of

that

statement

period);

Significantly, ANZ's above 'Definition' of

Closing Balance

does NOT include 'the amount of any

0% balance transfer' as a part of the

Closing Balance which

materially flaws ANZ reliance upon

page 10 of

"ANZ Credit

Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER CREDIT CARDS" [100 pgs] as part

of "Important things to know about using your ANZ credit card - Balance

transfers can affect how interest is charged on your credit card account"

which includes:

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account.

Whilst

interest

will

not

be

charged

on

the

0% balance

transfer,

interest

will

still

be

charged

in the

normal

manner

on

any

other

debits

to your

account. For

example,

interest

will

be

charged

on

your

purchases

balance,

except

to the

extent

an interest

free

period

applies."

The

amount of the

0%

balance

transfer

will

be included

in the

Closing

Balance

shown

on

a relevant

statement

of

account. Accordingly, an interest

free

period

will

generally

not

apply

in relation

to relevant

purchases

if

you

do

not

pay

the

full

Closing

Balance

(including

the

0%

balance transfer)

for

such

a

statement

of account

by the applicable

DUE

DATE.

Below is an extract from page 8 of ANZ's

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS":

"Understanding

interest

and

interest

free

periods

Interest

free

periods

on

purchases

We offer credit card

accounts with interest free periods on purchases and some credit card

accounts without. If you’re unsure whether your account has interest

free periods on purchases please refer to your Letter of Offer.

If your account has interest free periods on purchases, you can avoid

paying interest on the purchases balance by always paying the full

Closing Balance shown on each statement of account by the applicable DUE

DATE."

Having regard to the afore-mentioned inconsistencies about what indebtedness

constitutes the

Closing Balance, any prospective

Cardholder of an ANZ First Visa Card is entitled to

believe that if it pays the

Closing Balance as defined above that it

would

enjoy "Up

to 44 days interest free on purchases3. as asserted in

its webpage at 'Features and benefits' below. But that is

not the case.

Little wonder that ANZ notes

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account

because ANZ has advertised that

"Up

to 44 interest free days on purchases3

if the

Closing Balance is paid by the 'Due Date'.

ANZ has patently breached

its obligations pursuant to

Regulation 28LFA

of the

National Consumer Credit

Protection Amendment

(Home Loans and Credit

Cards) Act 2011 (Cth) Division 3, ss133BB‐133BD

which were introduced by

the Gillard Govt on 1 July 2012 because

ANZ's

Key Facts Sheet titled "Key facts about our credit cards"

-

A.

notes at

Interest-free period "Up to 44 days on the purchases

balance"; and

B.

does not alert that this

Interest-free period on Purchases is

not available whilst any of the 'Balance Transfer' remains unpaid.

Consumer Credit Reform and Behavioural Economics: Regulating Australia’s Credit Card Industry written

by Paul Ali, Cosima McRae and Ian Ramsay explains on its page 13:

" Regulation 28LFA

requires lenders to provide a Key Fact Sheet ("KFS") at the time

an application for a credit card is made by a consumer. The KFS must be contained on the application form

itself, or given to the consumer on a separate piece of paper with the application and the lender

cannot merely refer to a website. Critically, credit card fees, charges and interest rates are unbundled with

the specification of a plain language, large font table that separates fees, interest rates, minimum

repayments and other charges. This ‘unbundling’ of fees and charges addresses the optimism bias by

separating the short term low costs (teaser fees and introductory rates) from longer term interest

rates applying to balances. The timing of disclosure occurs before the contract is signed, which may alter

behaviour by prompting the consumer to assess realistically their capacity to repay."

ANZ has been mischievous in its

Key Facts Sheet for

its

First Visa Card whereupon too many new customers with a

Balance Transfer have believed that they would enjoy an

Interest Free Period

on

Purchases provided they have paid their

Closing Balance

(defined above)

by the

Due Date.

A Word file version

of above 'Important information' in a jpg file is immediately below with pertinent

text for ANZ First Visa card in

yellow highlight.

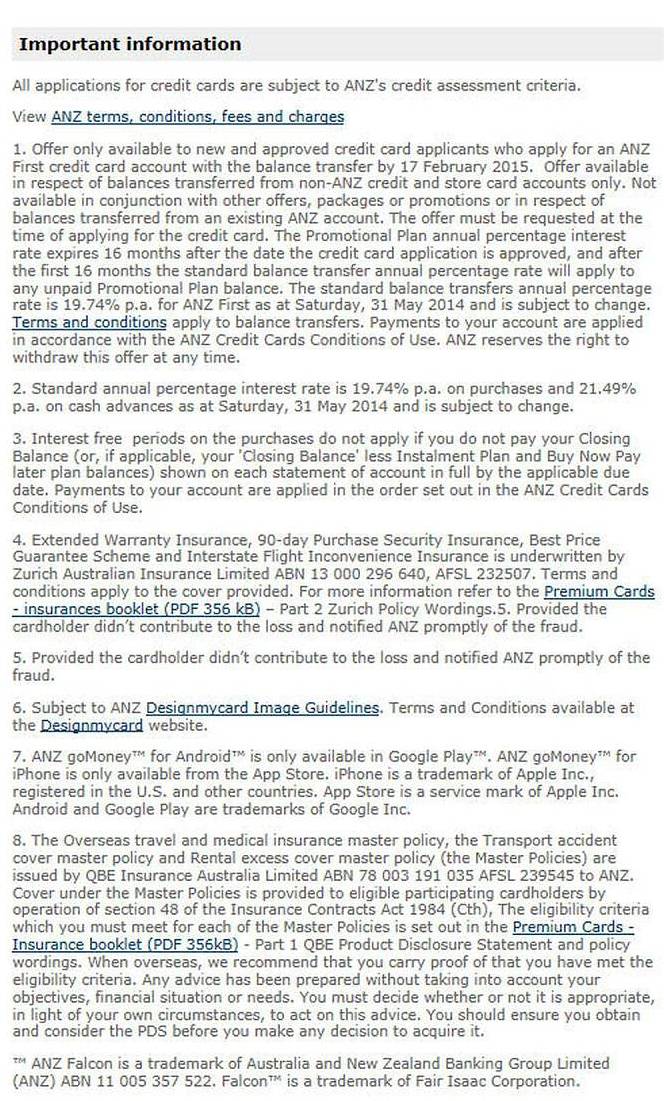

Important information

All applications for credit cards are subject to ANZ's credit

assessment criteria.

View

ANZ terms, conditions, fees and charges

1. Offer only available to new and approved credit

card applicants who apply for an ANZ First credit card account

with the balance transfer by 17 February 2015. Offer available

in respect of balances transferred from non-ANZ credit and store

card accounts only. Not available in conjunction with other

offers, packages or promotions or in respect of balances

transferred from an existing ANZ account. The offer must be

requested at the time of applying for the credit card. The

Promotional Plan annual percentage interest rate expires 16

months after the date the credit card application is approved,

and after the first 16 months the standard balance transfer

annual percentage rate will apply to any unpaid Promotional Plan

balance. The standard balance transfers annual percentage rate

is 19.74% p.a. for ANZ

First as at Saturday, 31 May

2014 and is subject to change.

Terms

and conditions apply to balance transfers. Payments to your

account are applied in accordance with the ANZ Credit Cards

Conditions of Use. ANZ reserves the right to withdraw this offer

at any time.

2. Standard annual percentage interest rate is

19.74% p.a. on purchases

and 21.49% p.a. on cash

advances as at Saturday, 31 May

2014 and is subject to change.

3.

Interest free periods on the purchases do not apply if you do

not pay your Closing Balance (or, if applicable, your 'Closing

Balance' less Instalment Plan and Buy Now Pay later plan

balances) shown on each statement of account in full by the

applicable

Due Date. Payments to your account are applied in the

order set out in the ANZ Credit Cards Conditions of Use.

4. Extended Warranty Insurance, 90-day Purchase

Security Insurance, Best Price Guarantee Scheme and Interstate

Flight Inconvenience Insurance is underwritten by Zurich

Australian Insurance Limited ABN 13 000 296 640, AFSL 232507.

Terms and conditions apply to the cover provided. For more

information refer to the

Premium Cards - insurances booklet (PDF 356 kb) – Part 2

Zurich Policy Wordings.5. Provided the cardholder didn’t

contribute to the loss and notified ANZ promptly of the fraud.

5. Provided the cardholder didn’t contribute to

the loss and notified ANZ promptly of the fraud.

6. Subject to ANZ

Designmycard Image Guidelines. Terms and Conditions

available at the

Designmycard website.

7. ANZ goMoney™ for Android™ is only available in

Google Play™. ANZ goMoney™ for iPhone is only available from the

App Store. iPhone is a trademark of Apple Inc., registered in

the U.S. and other countries. App Store is a service mark of

Apple Inc. Android and Google Play are trademarks of Google Inc.

8. The Overseas travel and medical insurance

master policy, the Transport accident cover master policy and

Rental excess cover master policy (the Master Policies) are

issued by QBE Insurance Australia Limited ABN 78 003 191 035

AFSL 239545 to ANZ. Cover under the Master Policies is provided

to eligible participating cardholders by operation of section 48

of the Insurance Contracts Act 1984 (Cth), The eligibility

criteria which you must meet for each of the Master Policies is

set out in the

Premium Cards - Insurance booklet (PDF 356kB) - Part 1 QBE

Product Disclosure Statement and policy wordings. When overseas,

we recommend that you carry proof of that you have met the

eligibility criteria. Any advice has been prepared without

taking into account your objectives, financial situation or

needs. You must decide whether or not it is appropriate, in

light of your own circumstances, to act on this advice. You

should ensure you obtain and consider the PDS before you make

any decision to acquire it.

™ ANZ Falcon is a trademark of Australia and New Zealand Banking

Group Limited (ANZ) ABN 11 005 357 522. Falcon™ is a trademark

of Fair Isaac Corporation.

After telephoning 3 staff on ANZ's Help Desk #

1800050.967, the Writer established that ANZ relies upon

"ANZ Credit

Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER CREDIT CARDS" [98 pgs],

specifically "Important things to know about using your ANZ credit card"

(page 7) which leads to the below extract of "Balance

transfers can affect how interest is charged on your credit card account"

on page 10. The first and third person the

Writer spoke to said

they wanted to check with their central control. They both returned a few

minutes later and told the Writer

that any unpaid Balance Transfer was included

in the calculation of the

Balance Transfer. The second Help Desk chap

that I spoke to, Phil, was adamant that '44 days interest free on purchases'

applied even with an outstanding

Balance Transfer.

Above is a jpg file of page 10 of

"ANZ Credit

Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER CREDIT CARDS" [100 pgs] as part

of "Important things to know about using your ANZ credit card - Balance

transfers can affect how interest is charged on your credit card account".

A Word file version

of above page 10 in an jpg file is immediately below with pertinent text re

interest on Purchases where a balance transfer remains unpaid for the ANZ First

Visa card in yellow

highlight.

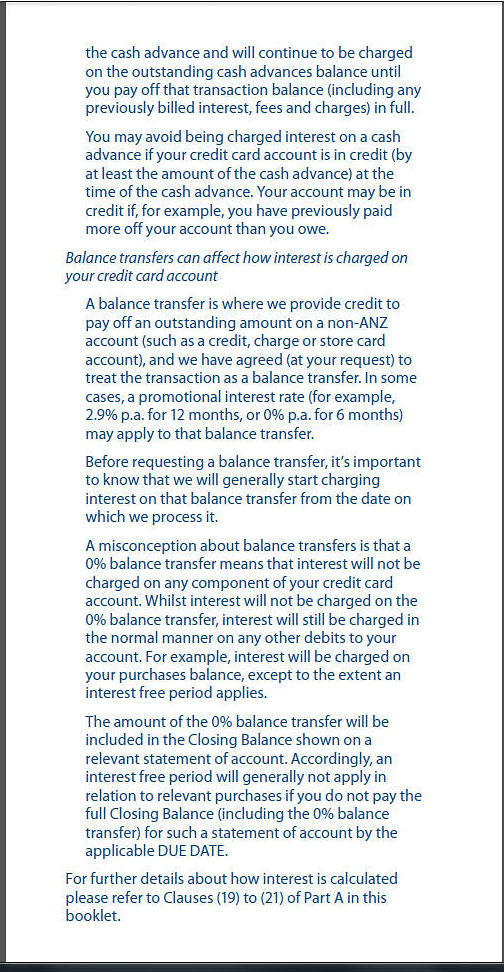

Balance

transfers

can

affect

how interest

is

charged

on your

credit

card

account

A

balance

transfer

is

where

we

provide

credit

to

pay

off

an

outstanding

amount

on a

non-ANZ

account

(such

as a credit,

charge

or

store

card

account),

and

we have

agreed

(at your

request)

to treat the

transaction

as a

balance

transfer.

In

some

cases,

a

promotional

interest

rate

(for

example,

2.9%

p.a.

for

12

months,

or

0%

p.a.

for

6

months) may

apply

to

that

balance

transfer.

Before

requesting

a

balance transfer,

it’s

important

to

know

that we

will

generally

start

charging interest

on

that

balance

transfer

from

the

date

on

which

we

process

it.

A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account.

Whilst

interest

will

not

be

charged

on

the

0% balance

transfer,

interest

will

still

be

charged

in the

normal

manner

on

any

other

debits

to your

account. For

example,

interest

will

be

charged

on

your

purchases

balance,

except

to the

extent

an interest

free

period

applies.

The

amount of the

0%

balance

transfer

will

be included

in the

Closing

Balance

shown

on

a relevant

statement

of

account. Accordingly, an interest

free

period

will

generally

not

apply

in relation

to relevant

purchases

if

you

do

not

pay

the

full

Closing

Balance

(including

the

0%

balance transfer)

for

such

a

statement

of account

by the applicable

DUE

DATE.

For

further

details

about

how

interest

is

calculated please

refer

to Clauses

(19)

to

(21)

of

Part A in

this booklet.

|

The Writer's comments:

Presentation of ANZ's webpages evidences that many Australians with

level 1 and level 2

Financial Literacy would be mislead to

believe that they will receive "Up

to 44 interest free days on purchases3".

The above

text on page 10 of ANZ's 98

pages

"ANZ Credit Cards -

CONDITIONS OF USE | 19.09.2014 CONSUMER CREDIT CARDS"

which includes

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account." is patent evidence that

ANZ has sought to deceive prospective users of amongst other Credit

Cards, it First

Visa Card that seek to park their debt at 0% for 16 months and believe

from ANZ's advertising information that they

will enjoy "Up to 44 interest free days on

purchases3".

Some other

Credit Card Providers overtly point out that the

Balance Transfer indebtedness negates any

Interest Free Period:

1. NAB's webpage

Balance transfers notes:

|

|

{kind=link}