Bankcard was launched in 1974. The RBA set the maximum interest rate that could be charged on Purchases and Cash Advances at 18%. The 18% Interest Rate Cap on all Credit Card Purchases and Cash Advances in Australia was removed in April 1985 following the Campbell Report when the Overnight Cash Rate was 17.2% circa.

Prior to the Campbell Report circa early 1980's, the RBA regulated all bank interest rates with an Iron Fist. The Overnight Cash Rate sat at 0.10% for 18 months from 4 Nov 2020. A far cry from the ultra high interest rates in the 1970s and 1980s.That maximum interest rate Cap on Credit Cards had stood at 18% until it was removed in April 1985 during a period of hyperinflation when the spread/margin between Overnight Cash Rate and that 18% interest rate Cap was less than 1%.

Australia's Principal Regulator of the Payments System

possessed and exercised 'extensive powers' under Section 50 of the Banking Act 1959 to regulate/Cap bank deposit/investment/loan interest rates from 1969 to 1980.Until 1980 banks could not offer more than 3¾% on a passbook account and 6½% interest on a Savings Investment Account (minimum account balance of $500, deposits and withdrawals must be $100 or greater, and 7 days written notice had to be given to the bank for all presently sought withdrawals). Leading up to 1980, building societies, finance companies and credit unions (unregulated) were offering materially higher interest rates and attracting bank customers deposits 'in droves'.

Bankcard was launched in 1974. The RBA set the maximum interest rate that could be charged on Purchases and Cash Advances at 18%.

In April 1985 following the Campbell Report the RBA removed the 18% interest rate Cap on Credit Cards when the Overnight Cash Rate was 17.2% circa. Hence, the spread was less than 1%.

The below four quotes from "Overview of Financial Services Post-Deregulation" by (Dr) Diana Beal, Director, Centre for Australian Financial Institutions, University of Southern Queensland, evidence that the Reserve Bank rigorously regulated bank deposit rates until 1980 when restrictions on interest rates were dismantled after adopting Campbell Committee recommendations:

"Interest-rate ceilings on deposit accounts restricted the banks’ ability to attract funds particularly during the 1970s when inflation was rampant. In the June quarter of 1975, inflation rose to 16.9% pa. At the same time, interest payable on amounts held in savings accounts offered by savings banks, for example, was restricted to 3.75% from 1969 to 1980 (Foster, 1996). In contrast, the interest rates offered by non-bank financial institutions (NBFIs) were not controlled and they were able to pay around 10% on passbook accounts."

"Banks in 1980 still operated in a highly regulated environment which was an artefact of previous economic and social conditions. Indeed, an extensive collection of controls remained from regulation introduced under the National Security Regulations in 1941."

"Interest rate ceilings on trading bank and savings bank deposits were dismantled from 1980; some limits on minimum and maximum terms on fixed deposits remained."

"The maximum interest rate payable on small balances in savings accounts was fixed by regulation at 3.75% from 1969 to 1980."

The Campbell Committee was established in 1979 and reported in 1981. The

recommendations of the inquiry were targeted at ..... the abolition of direct

interest rate and portfolio controls on financial institutions.

Campbell did not recommend

removal of any powers held by the Reserve Bank to regulate

interest rates or demand financial information. The Campbell recommendations were made following an

extended period of high interest rates. High deposit interest rates by

NBFIs existent circa 1980 are no longer an impediment to regulating credit card interest rates.

The abovementioned reference to Chapter Nine (in

Chapter 15 above): 'Stability and Payments'

of the Wallis Enquiry noted

"the RBA should retain overall

responsibility for the stability of the financial system, the provision of

emergency liquidity assistance and for regulating the payments system."

===========================

For 18 months from Nov 2020 to May 2022 the Overnight Cash Rate

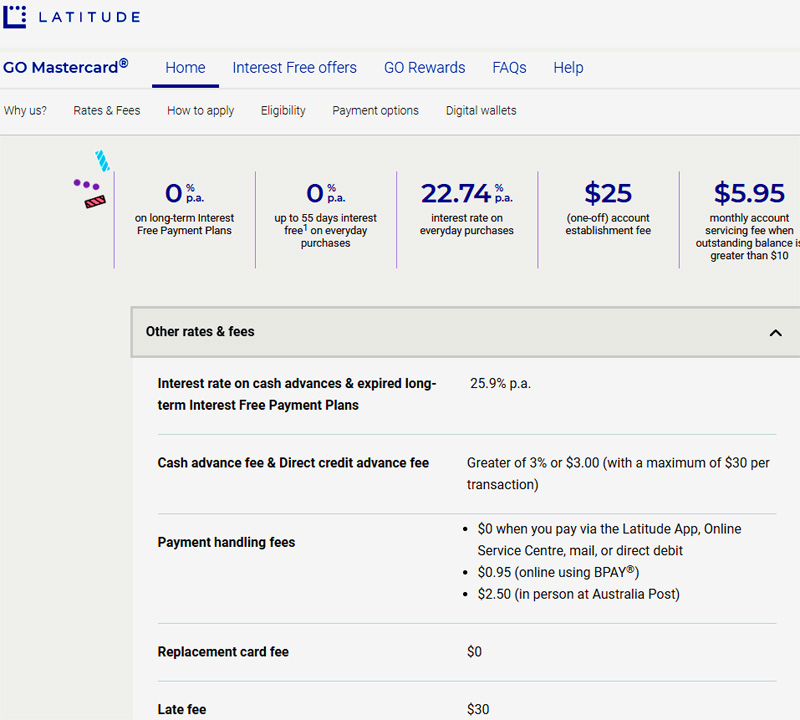

was only 0.10%. As at 29 Nov 2022 it was 2.85%.Currently the highest Cash Advance interest rate (Latitude Financial's Go Mastercard) is 25.9%. It also charges an explicit 'Late fee' of $35 and $8.95 monthly account service fee when the outstanding balance is greater than $10.

{kind=link}

"Australia’s most predatory credit cards revealed" - The New Daily - - George Lekakis

Highest Interest Rate Credit Cards - 25 April 2016

The 10 costliest credit cards in Australia - and why you should avoid them - Andy Kollmorgen - CHOICE - 17 June 2020