Interest Income And Late Payment Fees From Credit Cards means that the 80 - 20 Rule (Pareto Principle) applies to Credit Card Issuers' primary revenue source.

The Senate - Economics References Committee's submission "Interest rates and informed choice in the Australian credit card market" - December 2015 notes:

"2.9 While the RBA advised that about 75 to 80 per cent of credit card transactions do not accrue interest, about 65 per cent of the total quantum of credit card debt (or, as noted above, $33.1 billion) is accruing interest. To clarify, interest paying cardholders 'account for about 30–40 per cent of accounts, about 20–25 per cent of transactions, but close to two-thirds of the outstanding stock of debt'.9

20% of Cardholders that are Financially Uneducated And Vulnerable Australians, pay over 80% of Interest Income and Late Payment Fees. Put another way, 20% of Credit Cardholders pay over 80% of Credit Card Issuers operating costs which includes the cost of Rewards Schemes that the Financially Educated enjoy at no cost.

The User Pays Principle which is applies in over 95% of financial dealings in Australia (eg. filling up the tank with petrol, going to the movies, buying a case of beer, paying the electricity bill, catching the bus to work, paying the rent or mortgage payment) is non-existent when enjoying a Line/s Of Credit with a Credit Card/s. Net Interchange Fee income is immaterial to the P&L of a Credit Card Issuers.

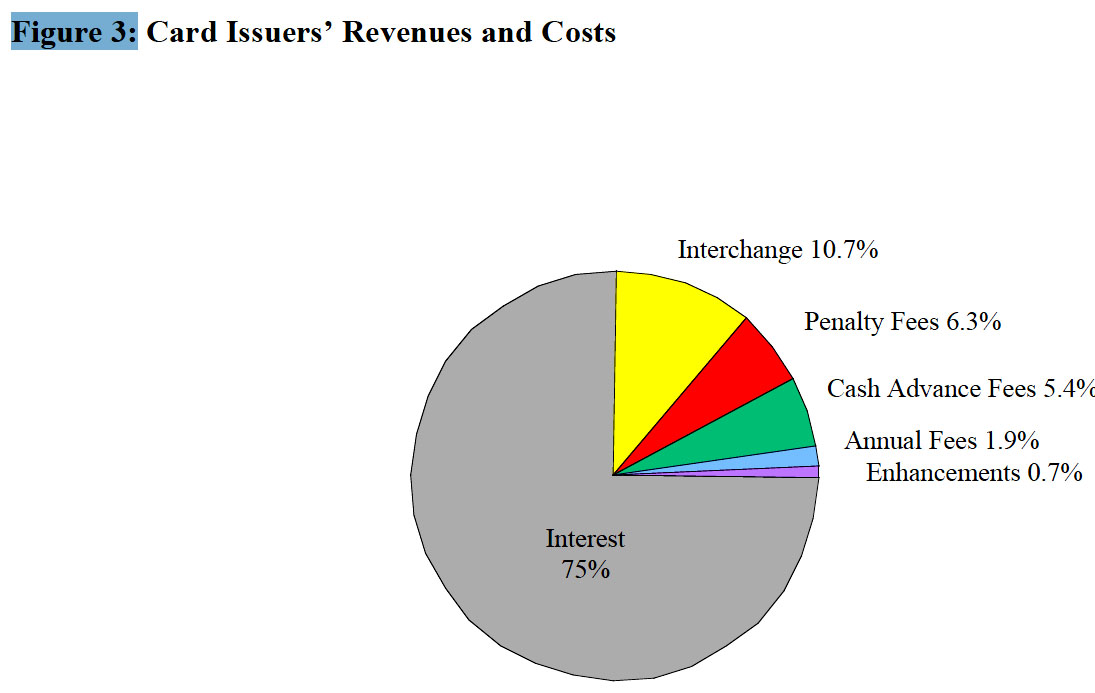

Figure 3 above is displayed in Who Pays for Credit Cards? by Sujit Chakravorti (Federal Reserve Bank of Chicago) and William R. Emmons - Federal Reserve Bank of St. Louis February 2001. The above 'pie chart' shows that Interest Income accounts for 75% of Credit Card Issuers net Revenues. Penalty Fees (Late Payment Fees) is a further 6.3% of Revenues, Net Interchange Fees are only 10.7% of Revenues. The high 75% being Interest is notwithstanding the below comment by the RBA that Interchange Fees are materially higher in the US than Australia, and would therefore :

So in Australia, where the RBA has materially pegged Interchange Fees (see quote immediately below), the percentage of Net Revenue from Interest and Late Payment Fees is likely to also exceed 80% of Total Net Revenues.

“What are the RBA's new interchange standards?

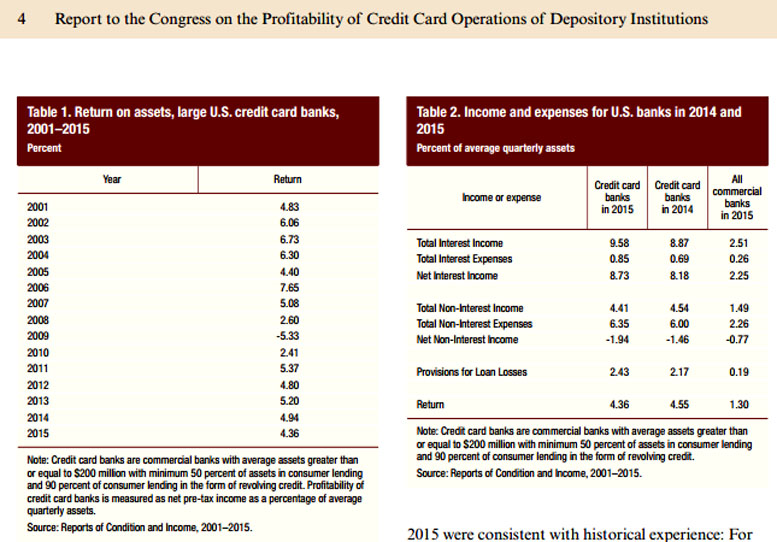

The U.S. Federal Reserve's annual Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions - June 2016 includes the below Table 2 which shows that 'USA Credit Card Banks' in 2015 had Net Interest Income of 8.73% and Net Non-Interest Income of -1.94% of average quarterly assets. USA Credit Card Banks are defined as commercial banks with average assets greater than or equal to $200 million with minimum 50 percent of assets in consumer lending and 90 percent of consumer lending in the form of revolving credit.