Estimated Current Annual Credit Card Interest Revenue is $3,889,869,715 circa calculated on the 'Value of credit and charge card balances accruing interest as at Sept 2022' of $18,092,417,278 in RBA Excel file c01hist.xlsx - Column Q Row 464 multiplied by the average interest rate levied of 21.5% p.a. that allows for the much higher interest rate on Cash Advances. This estimate does not include the 4% estimate of Credit Card Penalty Fees Revenue to gross Credit Card Revenue.

RBA worksheet 'Data' in Excel file c01hist.xlsx reports the 'Value of credit and charge card balances accruing interest as at Sept 2022' was $18,092,417,278 (cell Q464) interest accruing debt @ 21.5% ave interest rate. An average interest rate levied of 21.5% is chosen due to $5,079,735,886 (cell C464) [$5.08 bil) in Cash Advances drawn in the year to Sept '22 at a higher than Purchase interest rate.

Latitude Financial's Go MasterCard had a Cash Advance interest rate of 29.49% until March 2019. Presently it is 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. It also charges an explicit 'Late fee' of $35 and $8.95 Monthly Account Service Fee when the Outstanding Balance is greater than $10.

Citi Rewards Credit Card has a Purchase interest rate of 21.49% p.a., a Cash Advance interest rate of 22.24%, an Annual Fee of $149 p.a. after the 1st year, $90 p.a. for an additional card. Late Payment Fee of $30. Dishonour Fee of $15. Domestic Cash Advance Fee of 3.5% or $3.50 which ever is the higher. Overlimit Fee (for accounts opened prior to 1 July 2012).

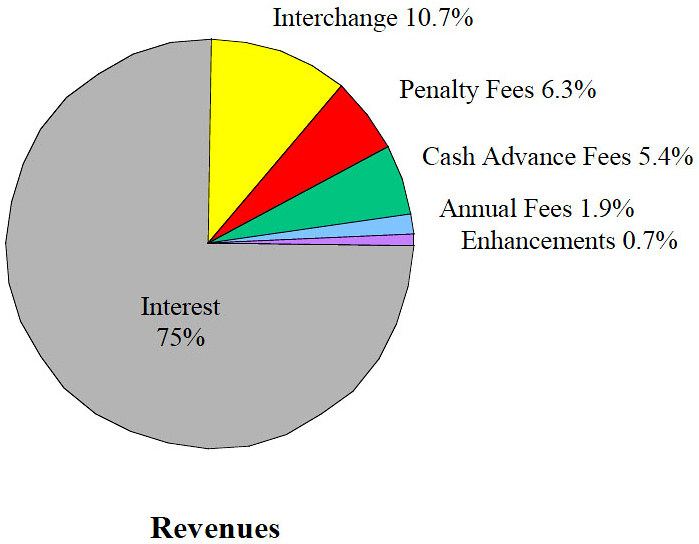

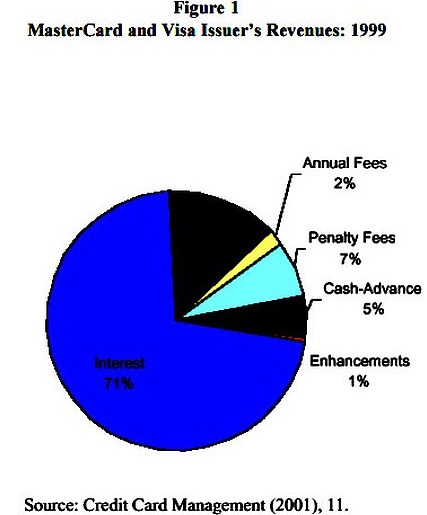

The above 'pie chart' appeared in a journal report titled "Who Pays for Credit Cards?" dated 2001 which displays a break-up of Card Issuers' Revenues for the aggregate of Visa, MasterCard and Discover cards in the USA. It shows that of Total Revenue, Interest Revenue was 75% and associated Penalty Fees Revenue (Late Payment Fees and Overlimit Fees) was 6.3% and Cash Advance Fees was 5.4% which aggregate to 86% of Card Issuers' Annual Revenues in the U.S.A. It does not identify % for Interchange Fees (in black) which seems to be 14%.

See: Interest And Penalty Fees Revenue