Defined Terms and Documents

Black marks mean higher borrowing costs - Choice - Last updated: 01 April 2014

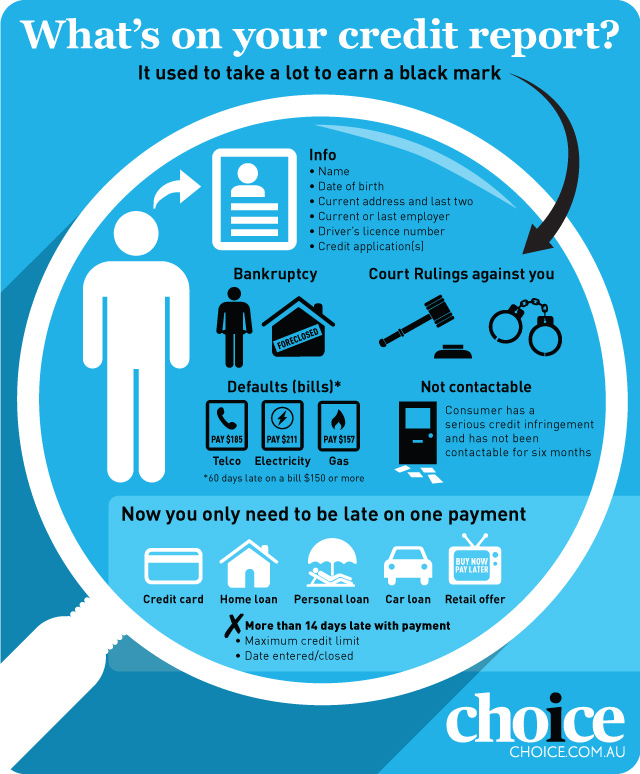

Until now, paying off your credit card two weeks late wouldn't have affected your credit rating. But that's about to change.

A new credit reporting regime which began on this year (2014) means credit card or personal loan payments made more than 14 days late will leave a black mark on your credit rating.

Before the change, only a string of missed payments that amounted to a

default would go on your credit report. This black mark could mean you'll be

charged a higher interest rate next time you apply for credit. The new payment history information on your

Credit Report will cover:

-

credit cards

-

car finance (car loans)

-

home loans

-

personal loans

-

store finance offers;

-

other types of consumer credit.

59% of Australians

don't understand how credit reporting works.

Late payments for utility bills such as electricity or phone will still only appear on your Credit Rating if you're 60 days or more late making the payment.

Your bank, credit union or other financial institutions can easily do a Credit Check when assessing an application for a credit card or home loan.

If these changes come as a shock to you, you're not alone. According to the Australian Retail Credit Association, 59% of Australians don't understand how credit reporting works, let alone being aware of these major changes.

Do a Credit Check and protect your credit rating

When you need a home loan, personal loan or car finance, you need it now, and a bad Credit Rating because of a mistake on your Credit File can mean a delay of a few weeks or months.

That's why it's a good idea to order your Credit Report regularly to make sure everything is up-to-date and your credit rating is not affected by incorrect information.

Your Credit History is held by private credit reporting agencies such as Veda and Dun and Bradstreet. The agencies don't make it easy but you can do a Credit Check for free every 12 months.

But beware:

These agencies also offer paid express credit ratings and other options, such as a credit alert or credit score. The paid services are advertised prominently on their websites, while the link to the free Credit Report is hidden.

-

You'll need to order your Credit File from each of the three national credit reporting agencies:

* Veda,

* Dun and Bradstreet; and

* Experian (as well as the Tasmanian Collection Service if you live in Tasmania).

-

These agencies also offer paid express credit ratings and other options, such as a Credit Alert or Credit Score. The paid services are advertised prominently on their websites, while the link to the free Credit Report is hidden. Use our buttons below to go straight to the right page. Many people have paid for their credit file unnecessarily: 43% of the respondents to a survey by the Office of the Australian Information Commissioner who had accessed their credit report had paid for it.

Veda and Dun and Bradstreet on notice

Credit reporting agencies, especially Veda and Dun and Bradstreet, are on notice to do a better job.

"One of the things we will be doing after the commencement of the [new credit reporting regime] is an assessment on how those types of organisation are meeting their requirements" says Privacy Commissioner Timothy Pilgrim.

CHOICE will be watching.

How to order your free credit report

Credit reporting agencies are required to make free credit reports available, but they don't always make this service easy to find. Click on the links to order your credit history from Dun and Bradstreet, Experian and Veda.

Black marks on your credit rating may mean your application for a credit card or home loan gets knocked back. This probably won't happen if the only problem with your credit rating is that you were 14 days late on a car loan payment. But you could still get penalised for making late payments.

"It's inevitably going to lead to those consumers being charged higher interest rates," says Katherine Lane, principal solicitor at the Consumer Credit Legal Centre.

What can you do?

Arrange a direct debit for at least the minimum payment on all your credit cards and other loans so that you can avoid late payments.

What information affects your credit rating?

Before 12 March 2014, only major infractions were noted on your credit report, such as dodging a bill altogether or paying your phone bill 60 days late. These are defined as defaults and will still go on your file, but now the unpaid bill will have to be at least $150 to count as a default, up from $100.

That's one of only a few minor wins for consumers, since the new regime will also keep track of a range of other information that was previously unrecorded, including:

-

the date a credit card or personal loan was opened and closed

-

the maximum credit limit

-

whether you made the minimum payment on time.

The same applies to mortgages, investment home loans, car loans and store finance offered by a licensed credit provider such as your bank or credit union. Whether or not you paid on time will be noted each month and the information retained for two years.

-

5 years is how long information about a bankruptcy stays on your credit report

-

5 years is also how long information about a payment default for consumer credit such as a credit card or utility bill of more than 60 days stays on your credit report.

-

2 years is how long information about a delay of more than 14 days in paying your credit card, home loan or personal loan stays on your credit report.

How to fix mistakes on your credit report

More information for credit reporting agencies means more opportunity for mistakes – and there were already plenty of them with the previous system:

-

30% of Australians who had ordered their credit report found mistakes in it in a 2013 survey by the Office of the Australian Information Commissioner.

-

Only 60% of people in the survey who found mistakes got them sorted out.

-

Order your free credit report once every year.

-

Check your credit history.

-

If there's a problem, contact the utility company or credit provider, or the credit reporting agency.

-

Once the problem is fixed, the credit reporting agency should notify you in writing.

-

If you're not satisfied with the dispute resolution scheme's decision, make a complaint to the Australian Information Commissioner.

If the problem on your credit file is not fixed, contact the relevant external dispute resolutions scheme – the utility company or credit provider and the credit reporting agency will be able to tell you the correct scheme.

Dispute resolution agencies for services providers:

See: