Writer's CD submission to RBA sent 8 Dec 2011 Defined Terms and Documents

From pizzas to credit cards - how to encourage better consumer behaviour – AFR – Chanticleer - TONY BOYD - 02 Jan 2019

When the British government last year proposed laws to cap the number of calories in a pizza at just under 1000 as a way of fighting the long-term costs to society of obesity, it resonated strongly with behavioural economists.

The calorie cap is just another way of nudging people to behave in a way that protects them from themselves while reducing the long-term costs to society from poor decision making. These policies are sometimes referred to as libertarian paternalism.

The idea, which was pioneered by behavioural economists, is to use rules, regulations and laws to affect human behaviour while respecting freedom of choice.

Michael Saadat, who is ASIC's executive director of financial services, led the investigation into credit cards.

A version of this is being implemented in the local credit card market after an Australian Securities and Investments Commission investigation, led by senior executive Michael Saadat, found credit card providers were exploiting customers to make higher profits.

ASIC has managed to convince the country's leading credit card issuers, including the big four banks and Citi, to voluntarily implement changes that should help consumers with problematic credit card debt, lead to fairer approaches for balance transfers and limit the amount by which consumers can exceed their credit card limits.

David Moloney, the founder of Internal Consulting Group and the head of its global financial services practice, says the changes being implemented fit with his analysis of the evolution of the financial system.

He says the financial system is going through three eras:

-

detriment reduction,

-

competition; and

-

the betterment of society.

He says the Hayne royal commission exposed the era when financial institutions sold products that were to the detriment of customers. Hayne will encourage, or possibly force, the financial sector to remove products that cause detriment to customers.

The competition era, according to Moloney, involves greater transparency about product pricing and more choices for consumers. It should involve lots more switching of customers from one product provider to another.

This era will benefit from -

-

open banking,

-

the sharing of data; and

-

the rise of fintech companies with access to personal banking data.

Delicate balancing act

The third era is arguably the most interesting because it will force banks and non-banks to think about products in a totally different way. Trying to act for the betterment of society while still responding to the demands of shareholders will be a delicate balancing act.

The credit card market provides the ideal case study for exploring Moloney's thesis because it would benefit from ending detrimental products, more competition and providers of credit acting for the betterment of society. Also, it is an example of the implementation of policies based on the principles of behavioural economics.

It is noteworthy that Hayne did not investigate the credit card market. Instead, he examined case studies where people took out personal loans they could not repay.

If Hayne had lifted the lid on credit cards he would have found the same awful, exploitative behaviour uncovered by ASIC. It is pretty clear that revolving debt on credit cards is a more deep-seated and widespread problem in society than personal loans.

The brutal reality is that credit card issuers, led by the big four banks and Citi, profit from a large proportion of their customers getting caught in the debt trap of revolving credit with interest rates as high as 23 per cent a year.

The ASIC deep dive into the use of credit cards followed evidence showing card issuers avoided warning customers about credit card repayment deadlines and actively encouraged them to take on more debt. It is in the interests of credit providers for consumers to miss deadlines and incur compounding interest payments.

ASIC found the majority of credit providers encouraged heavily indebted customers to take advantage of zero interest balance transfers. This was supposedly a way of getting on top of their debt problems. But the ASIC data showed that a third of all balance transfer customers increased their debt by more than 10 per cent and about 16 per cent later increased their total debt by more than 50 per cent.

The ASIC report painted a picture of an industry happy to have their customers incurring growing amounts of revolving debt. Non-bank providers were just as bad with their so called "interest free" purchase plans with high fees, penalty interest and balloon payments after a few years.

The credit providers use their own version of behavioural economics. They lead people to think they can have something they cannot afford. But instead of buying something to own, the consumer is paying to rent the product.

Struggling with debt

Many years ago credit providers forced credit card holders to repay 5 per cent of the outstanding amount per month as a minimum repayment. This forced repayment of a debt in about two years. The credit providers happily slashed the minimum repayment to 3 per cent, which led to exponential growth in interest paid and meant it took about 4½ years to repay the amount borrowed.

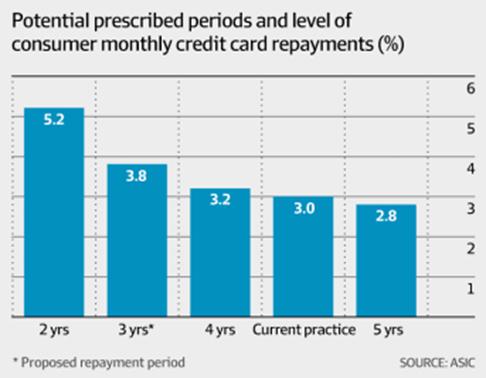

ASIC's analysis shows that if a consumer repays the credit limit within three years, they will pay interest charges equal to 37 per cent of the credit limit (compared to 25 per cent for repayments over two years). This amount increases to 51 per cent if a consumer repays the credit limit within four years, or 66 per cent over five years.

The ASIC report, which was published in July, found that one in six consumers struggled with credit card debt. As of June 2017, more than half a million Australians had overdue credit card debt, almost 1 million had persistent debt and 435,000 were repeatedly repaying small amounts.

David Moloney, the founder of Internal Consulting Group and the head of its global financial services practice, says the financial system is going through three eras: detriment reduction, competition and the betterment of society.

About $31.7 billion in credit and charge card balances were accruing interest as of October 2018, according to the latest Reserve Bank of Australia data. There is another $20 billion in credit and charge card debt that is paid off each month. These card holders are usually people who are well off and use their cards to generate reward points.

Last month, ASIC said it had made substantial progress in instituting reform. The 10 largest credit providers have voluntarily given commitments to change many of their practices.

Since July last year, ASIC has introduced its version of the pizza calorie cap. It has prescribed a three-year period for credit card responsible lending assessments. From this week, credit providers must not provide a credit card with a credit limit that the consumer could not repay within three years.

Credit providers have agreed to restrict the amount by which consumers can exceed their credit limit to 10 per cent. ASIC published a chart showing which credit providers are making changes and which are not. American Express stands out as a recalcitrant with no restrictions on exceeding credit card limits and no commitment to change to a fairer approach to balance transfers.

Threat to profitability

Commonwealth Bank of Australia, Citi and Westpac will promote structured payment arrangements for those with high levels of persistent credit card debt, while ANZ, HSBC and National Australia Bank will try to educate consumers.

ANZ, Macquarie and Westpac have already conducted piloting exercises for helping consumers deal with problematic credit card debt.

The idea of financial institutions acting for the betterment of society will be hard to implement because there is a threat to profitability.

Regulate

One way for banks to think about this issue is to consider the concepts of "good debt" and "bad debt". Credit card debt could easily be regarded as "bad debt" because interest rates are so high and repayment obligations can be kicked down the road.

It is possible to think of a mortgage as "good debt" because the consumer is saving for what should ultimately be an asset that will appreciate in value. With this in mind banks should encourage customers to ditch the bad debt and take up the good debt.

Many smart consumers pay off their credit card debt through a mortgage loan account because this is the lowest possible interest rate available to a consumer.

One obvious conclusion that can be drawn from ASIC's investigation is that products that force regular repayments and do not incur interest should be better for consumers.

The most popular product with these characteristics is Afterpay. It forces you to pay for the product in four equal instalments over a 56-day period. It works to the advantage of the consumer because if you do not repay you cannot buy anything more. CHARGE CARDS

With less than a month to go before the release of the final report of the Hayne royal commission, Australia's financial institutions ought to be thinking a lot more about how they can act for the betterment of society. They would be better off doing so without regulatory intervention.

Shocking indictment of the regulator oversight of the principal regulator of the payments system.