Defined Terms and Documents 'Aboriginal Teenager Life Skills' Social Inclusion Early Intervention Program

Cost-Benefit Analysis that -

A. accords with the reports and publications listed in Cost Benefit Analysis Knowledge and Expertise, that includes Regulation Impact Statement (described in the User Guide to the Australian Government Guide to Regulation) to assist Commonwealth, State and Territory governments to produce a Regulation Impact Statement (RISs) that meets best practice; and

B. includes a Base Case Financial Model .

Below are extracts from item 1 of Cost Benefit Analysis Knowledge and Expertise, namely Australian Government COST–BENEFIT ANALYSIS - Guidance Note - March 2020 - Department of Prime Minister and Cabinet - Office of Best Practice, which form the basis of a Conforming Cost-Benefit Analysis:

"The major steps in a cost–benefit analysis

Conducting a well-executed CBA requires you to follow a logical sequence of nine steps.

Step 1: Specify the set of options

Identify a range of genuine, viable, alternative policy options to be analysed. You must consider at least three options, one of which must be non-regulatory. Your agency is responsible for the choice of options. A ‘do nothing’ or ‘business as usual’ option will usually provide the base case against which the incremental costs and benefits of each alternative are determined. In some cases, doing nothing may be the best option available. Only costs and benefits that would not have occurred in the base case should be included in the CBA.

Step 2: Decide whose costs and benefits count

For most regulatory proposals, measuring the national costs and benefits is appropriate. That is, as far as is practical, you should count the costs and benefits to all people residing in Australia.

2Step 3: Identify the impacts and select measurement indicators

Identify the full range of impacts of each of the options. It is important to identify the incremental costs and benefits for each option, relative to the base case (which will normally be ‘what would happen if the current arrangements were to continue?’).

Where relevant, the base case should be forward-looking, recognising that the world in which the regulation will be implemented may differ from the current situation (key variables may change in the future, meaning that current or historical parameters may not be the most relevant benchmark). That is, the base case should not simply assume that nothing will change over time—changes that can be reasonably expected should be recognised when identifying impacts of each option.

All the effects of a proposal that are considered desirable by those affected are benefits; all undesirable effects are costs. CBA requires you to identify explicitly the ways in which the proposal makes individuals better or worse off.

The choice of indicators to measure the impacts depends on data availability and ease of monetisation. For example, a regulatory proposal may reduce risks of a hazard. Its positive impact could be measured in terms of a reduced number of accidents. The benefit from accidents avoided could be valued in dollars (see Step 5).

Step 4: Predict the impacts over the life of the proposed regulation

The impacts should be quantified for each time period over the life of the proposed regulation. The total period needs to be long enough to capture all the potential costs and benefits. Because of the uncertainty involved in forecasting costs and benefits over long periods, exercise caution when adopting an evaluation period longer than, say, 20 years (although some environmental regulation may merit the use of a longer time horizon).

Predicting future impacts is difficult. There will always be some uncertainty about the outcome of a proposed regulation. Conducting an assessment of uncertainties should be a standard component of the evaluation of any major proposal. This means that you assess expected values and variability of cost and benefit flows, as well as taking downside risks into account.

A CBA should present the best estimates of expected costs and benefits, along with a description of the major uncertainties and how they were taken into account. You need to set out how costs and benefits are likely to vary with general economic conditions and other influences. For example, would large relative price changes (such as a rise in energy prices or real wages) significantly change the net benefits from the regulatory proposal? If so, what price path might be expected? In general, your CBA should not just assume that the net benefits for one year will be repeated every year.

Although it is difficult to predict what the effects of a proposed regulation might be in 10 or 20 years—or in some cases, even to attach objective probabilities to various scenarios—decisions require some assumptions to be made. A CBA should make those assumptions transparent. When you explicitly consider and justify the assumptions underlying the forecasts, it improves implementation planning and identifies where more effort should be made to improve the analysis. It is a first step towards dealing with the uncertainties that the regulatory proposal may create.

Step 5: Monetise (place dollar values on) impacts

Assigning a net dollar value of the gains and losses of a regulatory initiative for all people affected is one useful way to measure the effects of a proposed change. Measurement of costs and benefits in this way is sometimes referred to as monetising costs and benefits.

The amount an individual would pay to obtain (or avoid) a change (if that were necessary or possible) is one measure of the value of that change to them. The value could be positive or negative depending on whether the change makes them better or worse off. Summing these values across all affected people gives the community’s total willingness to pay for the change. If the sum is positive, the change increases efficiency. The costs and benefits to all people are added without regard to the individuals to whom they accrue: a $1 gain to one person cancels a $1 loss to another.

This ‘a dollar is a dollar’ assumption enables resource allocation to be separated from distribution effects—or efficiency from equity effects. That does not mean that distributional considerations are unimportant or should be neglected. It means that they should be brought into account as a separate part of the overall analysis of the proposal in question—which may be more important than the resource allocation assessment, but should be distinct from it. Dealing with equity issues is discussed in more detail below in the ‘Accounting for equity’ section.

Dollar values can be estimated from observed behaviour. You can measure the value people place on something by observing how much they actually pay for certain goods or services, and the quantities of those goods and services that are consumed. Market behaviour reveals people’s valuations (or is at least a guide to them). For example, if a consumer pays $3.50 for a cup of coffee, the value they place on the coffee is at least $3.50 (it will likely be higher).

That said, monetisation, or more general quantification, can be difficult because impacts are sometimes uncertain, some are difficult to value in dollar terms, and some are both uncertain and difficult to value. Environmental goods or safety provisions are typical examples of goods that are difficult to place dollar values on, as they are typically not traded in markets.

3 Various methods for estimating the value of non-market goods and accounting for uncertainty in CBAs are outlined below in the ‘Dealing with costs and benefits that are difficult to value’ section.The fact that some impacts may be very difficult to quantify in dollar terms does not invalidate the CBA approach. In such cases, a detailed qualitative analysis will often be most appropriate in place of dollar values. Your qualitative analysis should be supported by as much evidence and data as possible to increase the transparency of the report and to assist the decision maker in choosing between alternative options.

Step 6: Discount future costs and benefits to obtain present values

Why discount?

The need to discount future cash flows can be viewed from two main perspectives, both of which focus on the opportunity cost of the cash flows implied by the regulation. The first perspective is the general observation that individuals prefer a dollar today to a dollar in the future. This is most obvious in the fact that banks need to pay interest on deposits to entice individuals to forgo current spending. This general preference for current consumption is known as the ‘rate of time preference’ and relates to all economic benefits (and costs), not just those that are financial in nature.

Since individuals are not indifferent between cash flows from different periods, those flows cannot be directly compared. For monetised flows to be directly comparable in a CBA, those costs or benefits incurred in the future need to be discounted back to current dollar terms. This reflects society’s preferences, which place greater weight on consumption occurring closer to the present.

The second perspective is that flows of costs and benefits resulting from a regulation also have an opportunity cost for investment. When regulations impose costs on individuals or businesses, those costs will need to be funded in some way. This funding imposes costs on the affected party, either through the interest paid for borrowing the money, or the returns forgone when the funds are not used for other purposes.

The regulation will therefore only be beneficial -

* when it provides a return in excess of the cost to society of deferring consumption, or

* of the return that could have been earned on the best alternative use of the funds.

By applying a discount rate to future cash flows, the required rate of return is explicitly taken into account in the net present value calculation.

Either approach demonstrates that the need to discount future cash flows can be viewed in terms of the opportunity cost of the cash flows, whether this is the cost of delaying consumption or the alternative investment opportunities forgone. Since most of the costs and benefits of regulatory proposals are spread out over time, and their value depends on when they are received, discounting is crucial to CBA.

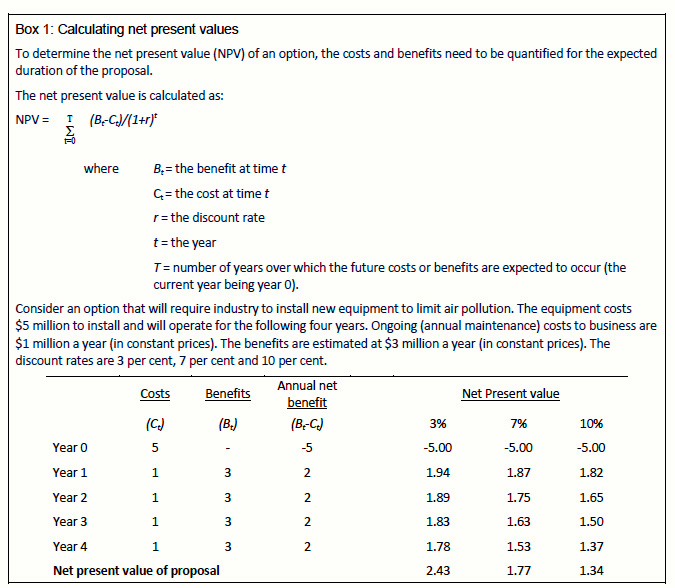

The rate that converts future values into present values is known as the discount rate. If the discount rate were constant at r per cent per year, a benefit of

Bt dollars received in t years is worth Bt/(1+r) t now. Box 1 provides an example of how to calculate net present values. The Handbook of cost–benefit analysis provides more guidance.4Accounting for inflation

Inflation is another reason that a dollar in the future is worth less than a dollar now. A general rise in the price level means that a dollar in the future buys fewer goods. Analysts conducting a CBA have the choice of whether to include future cash flows in terms of their actual monetary value at the future date (the ‘nominal’ value) or in terms of their current dollar value (the ‘real’ value). However, since all cash flows need to be converted to current dollar terms to be comparable in a CBA, it is usually simplest to adopt the latter approach.

CBA measures the value people place on various outcomes, preferably using their willingness to pay as revealed by their market behaviour. Consequently, the preferred approach is to base the discount rate on market-based interest rates, which indicate the value to the current population of future net benefits. Market interest rates determine the opportunity cost of any capital used by the Government’s regulatory proposal—that is, what it would have produced in its alternative use.

There is uncertainty about the appropriate discount rate to use for regulatory proposals. It is uncertain what the alternative uses for capital used by a proposal would have been, and what the capital would have produced in those uses.

The discount rate for regulatory interventions

Office of Best Practice Regulation requires the calculation of net present values at an annual real discount rate of 7 per cent.

5 As with any uncertain variable, sensitivity analysis should be conducted (see below for more information on sensitivity testing), so in addition to the 7 per cent ‘central’ discount rate, the net present values should also be calculated with real discount rates of 3 per cent and 10 per cent. If the sign of the net present value5 This is consistent with USOMB (2003) and NSW Treasury (2007), but below that recommended by Harrison (2010). Consistent with Harrison (2010), OBPR will accept analyses that use a central real discount rate of 8 per cent, with sensitivity analysis at 3 per cent and 10 per cent. Tt=0Σ changes, the sensitivity analysis reveals that the choice of discount rate is important. This information should be highlighted in the summary of the CBA, as it is an important caveat for the analysis.

In some cases, it may be desirable or appropriate to present the results of the analysis using another, different, discount rate. For example, if a well-known piece of international research uses a particular discount rate in presenting its results, it would be sensible to use the same discount rate in analysing Australia’s domestic impacts, to give a sense of the relative scope of the impacts in Australia compared to the results in the international study. Where there is a research-related reason for using a different discount rate, the analysis can be presented at that discount rate in addition to the 3, 7 and 10 per cent scenarios described above.

Harrison (2010), among others, provides a more detailed discussion of the issues surrounding the choice of discount rate.

Step 7: Compute the net present value of each option

The net present value (NPV) of an option equals the present value of benefits minus the present value of costs:

NPV = PV(B) – PV(C)

If the NPV is positive, the proposal improves efficiency. If the NPV is negative, the proposal is inefficient. If all costs and benefits cannot be valued in dollars, you should outline why the non-monetised costs and benefits are large or small relative to the monetised impacts.

Step 8: Perform sensitivity analysis

There may be considerable uncertainty about predicted impacts and their appropriate monetary valuation. Sensitivity analysis provides information about how changes in different variables will affect the overall costs and benefits of the proposed regulation. It shows how sensitive predicted net benefits are to different values of uncertain variables and to changes in assumptions. It tests whether the uncertainty over the value of certain variables matters, and identifies critical assumptions.

If sensitivity analysis is to be useful to decision makers, it needs to be done systematically and presented clearly. Common approaches to sensitivity analysis include the following:

• Worst/best case analysis: The base case assigns the most plausible values to the variables to produce an estimate of net benefits that is thought to be most representative. The worst, or pessimistic, scenario assigns the least favourable of the plausible range of values to the variables. The best, or optimistic, scenario assigns the most favourable of the plausible range of values to the variables. If the pessimistic scenario gives an NPV below zero, you will need to investigate the critical elements driving the value of the regulatory proposal, using the following two techniques.

• Partial sensitivity analysis examines how net benefits change as one variable varies over a plausible range (holding other variables constant). It should be used for the most important or uncertain variables, such as estimates of compliance costs, forecasts of benefits and the discount rate. It may be important to vary the values assigned to ‘intangibles’, especially when the assumed values are controversial. Partial sensitivity analysis clarifies for decision makers how the CBA results are affected by uncertainty about the level or value of a variable. If you find that varying a parameter has large effects on the net benefits from the proposed regulation, uncertainty about its value becomes important.

• Monte Carlo sensitivity analysis creates a distribution of net benefits by drawing key assumptions or parameter values from a probability distribution. See Boardman et al. (2010, pp. 181–184) for more details. While this is a more statistically robust approach to sensitivity analysis, care needs to be taken in adopting reasonable and justified assumptions about the probability distributions that have been assumed.

If the sign of the net benefits does not change after considering the range of scenarios, there can be confidence in the efficiency effects of the proposal.

Step 9: Reach a conclusion

You should summarise the results of the CBA. The option with the highest net benefit should be your recommended option. Given that NPVs are predicted (average) values, the sensitivity analysis might suggest that the alternative with the largest NPV is not necessarily the best alternative under all circumstances. For example, you might be more confident in recommending the option with a lower expected value of net benefits, but with a smaller chance of imposing a significant net cost on the community (lower ‘downside risks’).

Your conclusion should include the time profiles of costs, benefits and net benefits, their NPVs, the discount rate used, information on the sensitivity of estimated impacts to alternative assumptions, a list of assumptions made, and how costs and benefits were estimated.

Dealing with costs and benefits that are difficult to value

6When a proposal uses and produces goods sold in markets, estimating costs and benefits is in most cases conceptually more straightforward and is covered in a number of existing CBA guides.

7However, it is often difficult to identify and measure the effects of a proposed regulation, especially when there are impacts on goods not traded in markets, such as pollution levels and access to scenic views.

Costs and benefits can be difficult to value in dollars because their magnitude may be unknown or uncertain, or because they are difficult to express in money terms even if their impact is known. Examples include environmental, social and cultural considerations, regional impacts, health and safety, publicity, and national defence.

It is important that you identify and describe all costs and benefits. You should then quantify them as much as possible. When valuations are uncertain, sensitivity analysis should be used to test how varying the value assigned affects the overall viability of the proposal. If the impacts cannot be valued, they should still be quantified in non-monetary terms. For example, a regulation to reduce pollution could quantify the expected reduction in emissions. The quantification should aim to identify matters such as the assumptions applied to determine the effects, the impact on the community (such as how many people are affected and how) and the likelihood of the full impact being realised.

Where impacts cannot be valued, the reasons why that is the case should be set out clearly.

The process of trying to describe and measure costs and benefits is valuable in itself. By examining what determines the costs and benefits and how they are likely to vary, you should consider different approaches and determine the best way to achieve the intangible objectives. Is the policy the best way of producing them, or could a better outcome be produced by some alternative? Even qualitative descriptions of the pros and cons associated with a contemplated action can be helpful.

A wide range of tools have been developed to help you to estimate the value of costs and benefits when direct market information is not available, including revealed preference techniques and stated preference techniques. See Boardman et al. (2010) or Commonwealth of Australia (2006) for more information.

6 A more detailed explanation of these valuation methods and how they can be used in cost–benefit analysis is in a guidance note available from the OBPR website.

7 See, for example, Handbook of cost–benefit analysis, Commonwealth of Australia (2006, pp. 18–24).

Revealed preference techniques

Revealed preference techniques infer value from observed behaviour and market interactions. When individuals make purchases in markets, the price they pay reveals information about the value placed on that good. While this concept is useful for measuring the value of most markets, regulatory interventions typically deal with goods that are not directly traded in markets, or for which the market does not give a reliable signal as a result of one or more market failures. In these cases, estimating values to be included in a CBA will require that you consider non-market valuing techniques.

These techniques often require the use of market proxies to provide information on the value of a non-market good. When similar goods to the one being regulated are traded, their price will suggest the value placed on the good in question. For example, information about the benefit of providing free public transport can be gleaned from travel patterns in cities where citizens pay for this service.

Regulations that aim to reduce the probability of a negative event occurring can be valued by analysing the expense to which individuals previously went to avoid the event. For example, health and safety regulations often need to estimate the value of a statistical life. This value is often estimated by analysing expenditure on smoke alarms, car airbags and other devices that individuals buy to reduce the probability of death.

In some cases, the ‘price’ paid for a good might not be a physical exchange of money but instead reflect the effort and expense that individuals have incurred to consume the good. This expense can be used to estimate the value of a good when no explicit market is present. For example, the values of visits to galleries or museums can be estimated by analysing the travel costs of visitors and the opportunity cost of their time.

Stated preference techniques

In some situations, it may not be possible to use revealed preference techniques. These cases usually occur when a good is not actively consumed or enjoyed by individuals, but its mere existence is still valued. In such cases it is still possible to elicit information on the willingness of individuals to pay for a good by simply asking them to state their preferences. Stated preference techniques rely on surveys to obtain information on how people value costs and benefits. These surveys are called ‘contingent valuation’ surveys.

A survey may be the only way to collect information on non-use values where an individual places value on a resource or activity, even though they may not directly use it or participate in it, now or in the future. For example, people might be willing to preserve a wilderness area because they place value on knowing that some natural habitat exists for rare animal species.

Boardman et al. (2010, pp. 369–402) set out how to conduct contingent valuation surveys and outline some problems with the technique.

Choice modelling is another survey method that may be useful when the benefits from a proposal have many attributes and the options provide different combinations of those attributes. It is examined in Cost–benefit analysis and the environment: recent developments (OECD 2006, pp. 125–143).

To be a useful addition to a CBA, a stated preference study should aim to elicit willingness-to-pay estimates from well-informed individuals. For example, if a choice modelling study is trying to establish the community’s willingness to pay for a regulation to reduce a particular environmental risk, it is important that participants in the study base their responses on accurate information about the nature of the environmental risks, rather than on their uninformed perceptions of the risks. This underscores the importance of identifying, describing and, where possible, quantifying the likely impacts of a proposal.

As a general rule, estimates of individuals’ valuations of goods and services derived from observing their behaviour in markets tend to be more credible than those from survey questionnaires (Boardman et al. 2010). Observing purchasing decisions directly reveals preferences, whereas surveys elicit statements about preferences.

Survey respondents may have little incentive to take the question seriously, to invest in obtaining the information necessary to answer it accurately, or to be truthful. They bear little cost for inaccurate or ill-considered answers and may have an incentive to exaggerate.

Determining impact valuations from secondary sources

The methods discussed above provide a set of tools for the practical valuation of impacts, but may be difficult to implement. When you do not have the resources or expertise to conduct an original study, you may wish to ‘plug in’ values from previous studies. This process, called ‘benefit transfer’, has been used to estimate values such as the value of a statistical life or life-year, the value of travel time savings and the cost of noise and air pollution.

While information from secondary sources can provide a quick, low-cost approach for obtaining desired monetary values, you should treat it cautiously and not use it without a clear justification. Judgement is required to determine whether results from a previous study are appropriate to use in a particular RIS. Estimates gleaned from secondary sources may need to be adjusted, depending on the specifics of the particular application.

It is advisable that you carefully scrutinise the accuracy and quality of the original study. When studies with technical weaknesses are used, you should discuss any biases or uncertainties that may arise as a result. Clearly, if a study has major weaknesses, it should not be used. Furthermore, information from secondary sources is most robust when several sources can be used to corroborate the assumptions or estimates made. In this area, as in others, OBPR can provide assistance.

Dealing with costs and benefits that cannot be valued in dollar terms

Some costs and benefits resist the assignment of dollar values. A CBA should nevertheless include all relevant information that can affect a decision in such cases. It should make explicit allowance for costs and benefits that cannot be valued. You should report cost and benefit estimates within three categories:

• monetised

• quantified, but not monetised

• qualitative, but not quantified or monetised.

The challenge is to consider non-monetised impacts adequately. For example, if a proposal is advocated despite monetised benefits falling significantly short of monetised costs, the RIS should explain clearly why non-monetised benefits would tip the balance and the nature of the inherent uncertainties in the size of the benefits.

CBA can encourage decision makers to reveal the limits they place on non-monetised benefits. For example, the monetised costs of a proposed regulation may exceed monetised benefits by $23 million, which equates to a net cost of $1 per Australian resident over the life of the proposal. Is the non-monetised benefit valuable enough to outweigh the net monetised costs? It may be considered reasonable to assume that the residents value the proposal’s non-monetised benefits at more than $1 each. But if the cost were, say, $100 per head, it may not be plausible to assume such a high willingness to pay for the non-monetised benefits, depending on the benefits in question.

If quantification is not possible, your analysis should at least describe such intangibles in a qualitative manner and evaluate the strengths and limitations of the relevant arguments for taking those impacts into account. Where possible, include relevant data to support the qualitative analysis. For example, information on the number of people affected by the regulation or the value added of the affected industry may be useful to the final decision maker.

"