ALP turns blind eye to $88bn debt - The Australian - By JAMIE WALKER and and SEAN PARNELL - JUNE 12, 2019

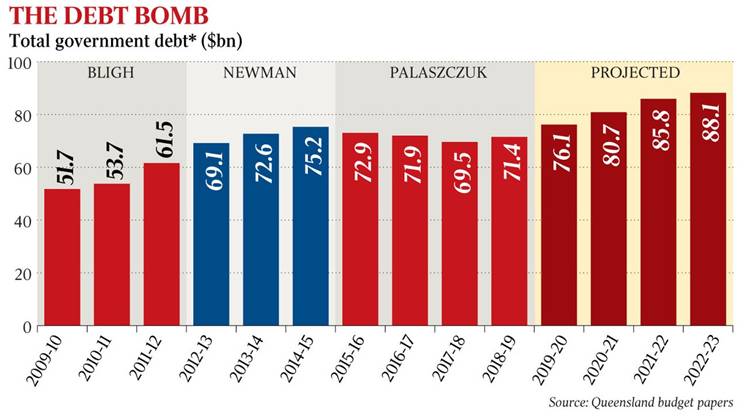

Queensland’s Labor government will continue to amass debt without paying down the $88.1 billion the state is forecast to owe within four years, kicking the problem into an uncertain economic future.

The mounting interest bill — $3.2bn this financial year, climbing to a projected $3.35bn in 2022-23 — is a drain on a budget struggling to accommodate record spending on health, education and a $49.5bn infrastructure program while delivering slender operating surpluses over the forward estimates.

Despite committing to debt reduction after it came to power four years ago, the government has now abandoned any pretence that it will try to make inroads into the nation-leading state debt, with Treasurer Jackie Trad pointing to other priorities.

“Our debt-reduction strategy aligns with our fiscal principles … maintaining surpluses, about ensuring we are tax competitive and growing the economy and to make sure the debt-to-revenue ratio is lower than what it was when we came to government,” she said.

Ms Trad told parliament the borrowings were affordable and necessary to fund job-creating infrastructure and capital projects that were underpinning the state economy.

The general public sector’s predicted debt-to-revenue ratio of 64 per cent for 2019-20 was down from a 91 per cent peak seven years ago and lower than any other major state except NSW, which had embraced the privatisation of electricity and other assets rejected by the Queensland government.

The budget papers assert that state debt will continue to balloon, albeit by slightly less than originally forecast. However, the government has taken advantage of new accounting standards to report a narrower definition of borrowings than previous years and strip out leases and other arrangements. From 2019-20, the separate lease component is also inflated by $2.2bn a year for the general government sector and $2.6bn for the non-financial public sector.

Although Ms Trad’s first budget in 2018-19 reported $32.3bn in government sector borrowing for the financial year now ending, that figure has been retrospectively split into three separate line items, the largest being $29.7bn raised through the Queensland Treasury Corporation. That is the only specific reference to “borrowing” on the new balance sheet, with the other line items reported as separate liabilities.

According to the budget, government sector borrowing through QTC is set to increase to $40.2bn in 2021-22.

However, combining the three separate line items used in the previous budget, and factoring in the leases change, puts comparable government sector debt at $45bn that year — $2.7bn more than forecast in the past budget. Across the non-financial public sector, using the same calculations, borrowings are forecast to be $2.7bn higher at $85.8bn and reach $88.1bn in 2022-23.

The changed accounting treatment, to bring Queensland in line with standards used elsewhere, will combine with falling growth in revenues and the timing of capital works and related borrowings to increase the debt-to-revenue ratio to 71 per cent over the forward estimates. This will stabilise in 2022-23.

While a surge in revenue allowed the government to avoid taking on more debt, that may not be sustainable, particularly if there is a deterioration in broader economic conditions.