The Drum David Taylor - 18 Feb 23

Lowe used his time in the parliamentary spotlight this week to double down on his resolve to squeeze millions of household budgets.

No one wants to be in a dentist's waiting room.

Why? Well because there's a better-than-even chance you're about to experience physical pain.

You could argue many Australian households are in that metaphorical waiting room right now, worrying about how much financial pain is heading their way.

The NAB's Alan Oster puts the odds of an Australian recession in the next 12 months at 51 per cent — just to emphasise the point that the risks have risen and there's now a better-than-even chance of an economic contraction.

Alan Oster, an economist at the NAB, puts the chances of a recession at more than 50 per cent.

What's shifted?

Nothing, except that after enduring intense pressure and criticism, far from retreating, the Reserve Bank has doubled down on its monetary policy agenda.

RBA governor Philip Lowe told Senate Estimates this week:

"I also want people to understand we're really serious about this.

"[Inflation is] too costly, too damaging, too corrosive.

"If people start to think inflation's going to be 7 or 8 per cent the year after next then we're going to have all sorts of trouble."

That has led a list of commercial and investment banks to forecast the Reserve Bank will need to raise its cash rate to 4.1 per cent or higher.

They're also worried about that interest rate outcome, and how much damage it could inflict on the economy.

"We are getting more concerned, though, that the RBA is raising rates too far in response to inflation which is a lagging indicator and is not paying enough attention to the lagged flow through of rate hikes to the economy and signs of slowing demand and improving supply which will push inflation down," AMP's chief economist Shane Oliver said.

"This is increasing the risk of a recession that we don't have to have and with that a bigger rise in unemployment and a bigger fall in home prices."

AMP's chief economist Shane Oliver is worried about the impact of more interest rate rises.

That's the other thing that's changed. The unemployment rate is now edging up.

So there's a lot of noise around inflation, interest rates, and the Reserve Bank — and it's left us in no doubt that the economy's slowing, perhaps quite markedly, and it's going to hurt some more than others.

But there's one major aspect of monetary policy that needs to be understood and resolved as a matter of urgency, and it may go some way to easing a bit of this pain.

Corporate profiteering and inflation

Let's quickly revisit what's causing this inflation, because we learned more this week.

We know demand and supply forces are driving the current soaring inflation.

The Reserve Bank has confirmed higher business costs (and businesses passing those costs on to customers in the form of higher prices) is driving the bulk of inflation.

We also know now that costs have actually been trending down for businesses, but they are yet to reduce their prices.

Our job is 'unpopular': RBA Governor Philip Lowe

"Importantly, survey measures of purchase cost and labour cost growth remain below their 2022 peaks and a downward trend still appears evident," the NAB noted this week.

The RBA governor confirmed to the House Economics Committee that firms are pushing prices as high as they can.

"When demand is strong you don't discount," Lowe said.

"And some firms no doubt take the opportunity to put up their price when demand is strong.

"That's how it works."

The problem here is that this profiteering may be occurring among firms delivering essential goods and services, items — like gas, for example — that some households cannot do without.

The Reserve Bank insists as interest rates keep rising, consumer demand will eventually fall, and firms will be forced to discount their prices.

It's unclear if this means some low-income households will endure a period of having to forgo basic items.

Unemployment on the rise

In any case, tens of thousands of households had to deal with a family member losing a full-time job last month.

Unemployment jumped from 3.5 per cent to 3.7 per cent in January, with the new Australian Bureau of Statistics data this week reminding us how vulnerable millions of families are to financial stress.

There was a bit of statistical "noise" in the numbers but the Treasurer drew the conclusion it was a sign that higher interest rates were now causing a degree of economic damage.

Economist David Bassanese said it showed the economy was beginning to "buckle".

This week MPs asked the Reserve Bank governor if this evidence would influence his interest rate decisions in the coming months and the answer was a resounding "no".

In short, he said the labour market was still "very tight" — meaning plenty of Australians still have the capacity to spend and drive inflation higher.

That is, the RBA governor is still proceeding on the basis that there's "strong demand" in the Australian economy.

The Reserve Bank doubles down

If anything, Lowe used his time in the parliamentary spotlight this week to double down on his resolve to squeeze millions of household budgets.

His reasoning for implementing an economic policy that's designed to inflict some degree of financial pain on households is sound. The alternative — allowing high inflation to fester — is far more painful for households because it leads to even higher interest rates and unemployment, he said.

"I know it's really hard for people to pay more on their mortgages but it'll be harder still if inflation gets too high and stays too high. It'll mean even higher interest rates and higher unemployment."

"It's hard for people to kind of understand that."

So what we've learned is that inflation is "way too high" and it needs to come down to avoid severe, widespread economic and financial pain.

The policy tool to control inflation is blunt and takes time to "kick in".

As it stands now though, the households carrying the financial burden of containing inflation are low-income households.

If Lowe was feeling the heat, he didn't show it - If Philip Lowe was feeling the heat at his Senate Estimates grilling on Wednesday, he didn't show it. For 90 minutes, he calmly explained why nine rapid interest rate rises, with the prospect of more to come, were the only way to go.

Lowe told MPs this week that all income segments are driving inflation, but wealthy households more so, and low-income families are disproportionately feeling the pain of rate rises.

This was new in terms of what we know about the "demand" landscape and a harsh reminder of the reality of a rising interest rate environment with low levels of wage growth and high levels of household debt.

Prosperous households are inadvertently pushing inflation higher and low-income households are paying the biggest price.

"It's hitting the wrong people," Labor MP Sam Rae told Lowe this week.

The RBA governor replied: "It's the only tool we have."

One obvious remedy

There's been some talk this week about alternative ways of reducing inflation, outside the limitations of monetary policy.

Fiscal policy has a role to play. The RBA governor said a much-reduced budget deficit would assist him in his role.

"If fiscal policy was tightened a lot, that would have implications for [interest rates], it's true," he told the House Economics Committee.

But there's one aspect of monetary policy that's not yet being fully implemented, and it would make some inroads into reducing its inequity and increasing its potency — deposit rates.

The first paragraph of the RBA's most recent statement read:

"At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 3.35 per cent. It also increased the interest rate on Exchange Settlement balances by 25 basis points to 3.25 per cent."

The second sentence has been rarely discussed. So, what are exchange settlement balances?

They're the commercial banks' deposit accounts with the Reserve Bank. The banks put their excess cash in these accounts every day.

By increasing the return on these accounts for the banks, the Reserve Bank opens the door for the banks to increase their own deposit rates on savings accounts.

More economic and business analysis

-

If Reserve Bank governor Philip Lowe was feeling the heat at his Senate Estimates grilling, it didn't show Author David Speers

-

Where can you get financial advice? A new report offers a good answer — and it's something I used to argue against By Peter Martin

-

Economists are suddenly beset with doubts about the relationship between jobs, wages and inflation Author - Ian Verrender

-

Instead of raising interest rates to kill spending, there are more creative ways to manage inflation Author Gareth Hutchens

-

It seems, as time moves on, that businesses are further fuelling inflation — not consumers Author David Taylor

-

The RBA has signalled it will keep pushing up rates — even if it means weaker economic growth By Peter Martin More Analysis

We know this aspect of monetary policy is not functioning as it should. Its weak flow-through is potentially pushing mortgage rates higher than they need to be.

It's also robbing millions of bank customers of potential savings — money that ends up in the banks' coffers instead.

The Commonwealth Bank's record profit was generated in part due to growing its deposit base to 75 per cent, where it pays less to depositors than it charges out to borrowers.

The Reserve Bank says as much as 15 per cent of savings pay zero interest.

"When we put up interest rates the immediate effect, I think, is a boost to bank profits — particularly if they're slow in raising deposit rates, which they have been," Lowe said.

"And I know the government is concerned about that and rightly."

"The banks earn more profits.

"My advice is to switch [banks]."

"There are some good deals out there and people should hunt them."

Australian households hold more than $1.3 trillion in savings and deposit accounts.

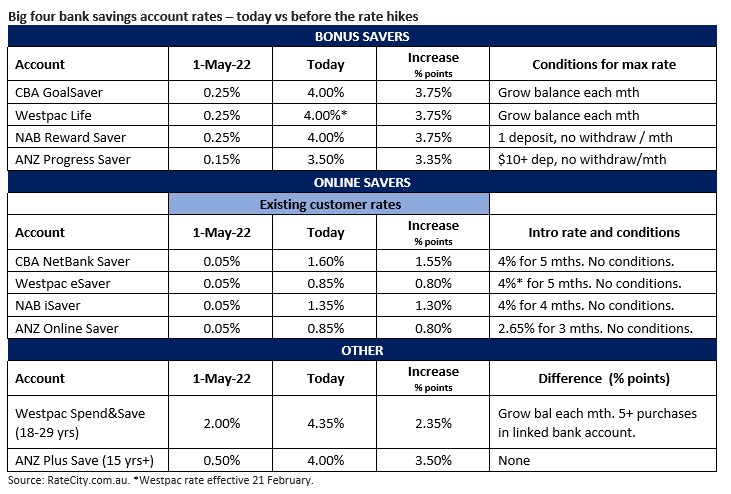

Interest rate comparison website RateCity said bank customers should be looking for a deposit rate with a 4 in front of it.

"While some banks have increased rates beyond the RBA's 0.25 percentage point rise this month, what ultimately matters is what rate customers are receiving on an ongoing basis.

Big four banks saving accounts rates. (Source: RateCity.com.au)

"Customers should be aiming for an ongoing interest rate that's at least 4 per cent, while keen savers can now get ongoing rates of up to 4.80 per cent.

"On this measure, a number of the big four bank savings accounts continue to fall short."

On Wednesday, Treasurer Jim Chalmers released the direction he gave to the Australian Consumer Competition Commission (ACCC) to investigate the timing of when the banks raise interest rates for savers.

The ACCC will report to the Treasurer by December and is expected to release an issues paper in the coming months, putting the banks on notice.

But while other solutions are investigated, more households are being swept up in this latest rising interest rates tsunami and all we can do is watch it coming at us.