Credit card holders gouged more than $2 billion since 2011, research shows

August 4, 15 View more articles from

The major banks are being accused of gouging customers with startling high interest rates. Photo: Jessica Hromas

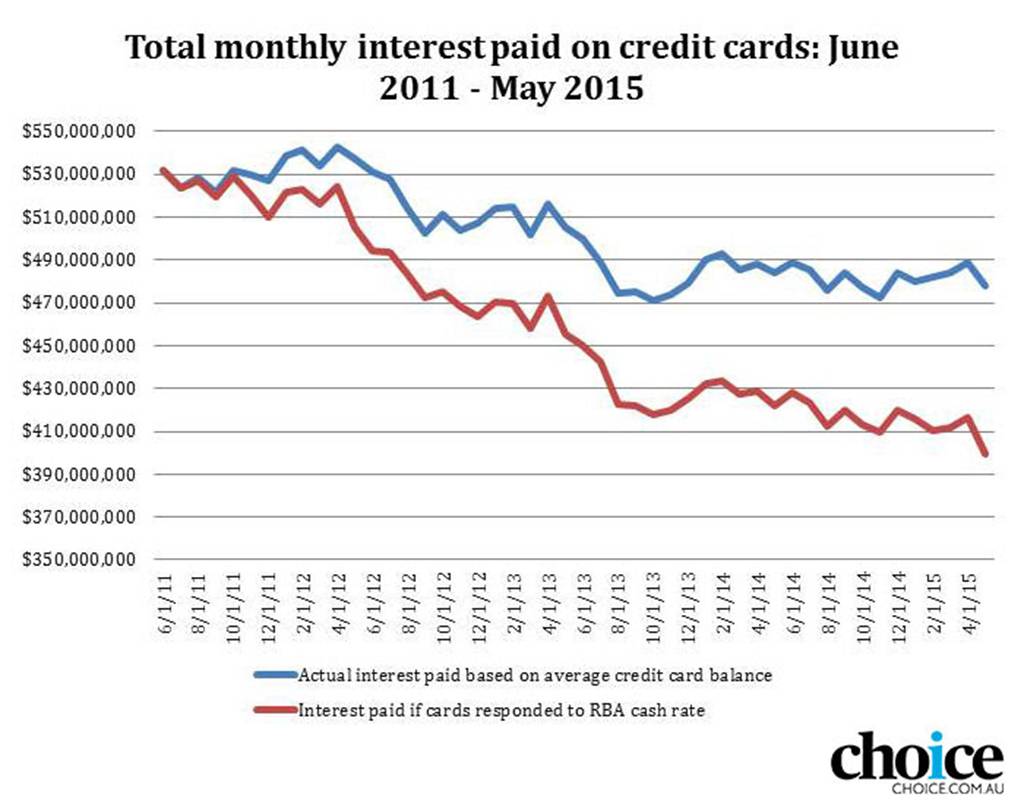

Credit card holders have been ripped off more than $2 billion dollars in nearly half a decade because of the banks' failure to pass on official interest rate cuts, research shows.

Since November 2011, when credit card providers stopped moving interest rates in line with the official cash rate, Australians have been gouged $2.07 billion, say consumer group Choice and comparison website Mozo.

"The fact is an average credit card holder has paid an extra $281 because of unnecessarily high interest rates. Worryingly, this comes at a time when one-in-five Australians are living off their credit card to get through to payday," said Choice's campaigns manager Erin Turner.

"The findings point to a systemic issue with Australia's banking system. Because the big banks control over 80 per cent of the credit card market, they aren't competing on price and are keeping consumer costs high even though their costs for providing credit have dropped," she said ahead of the Reserve Bank's meeting on Tuesday.

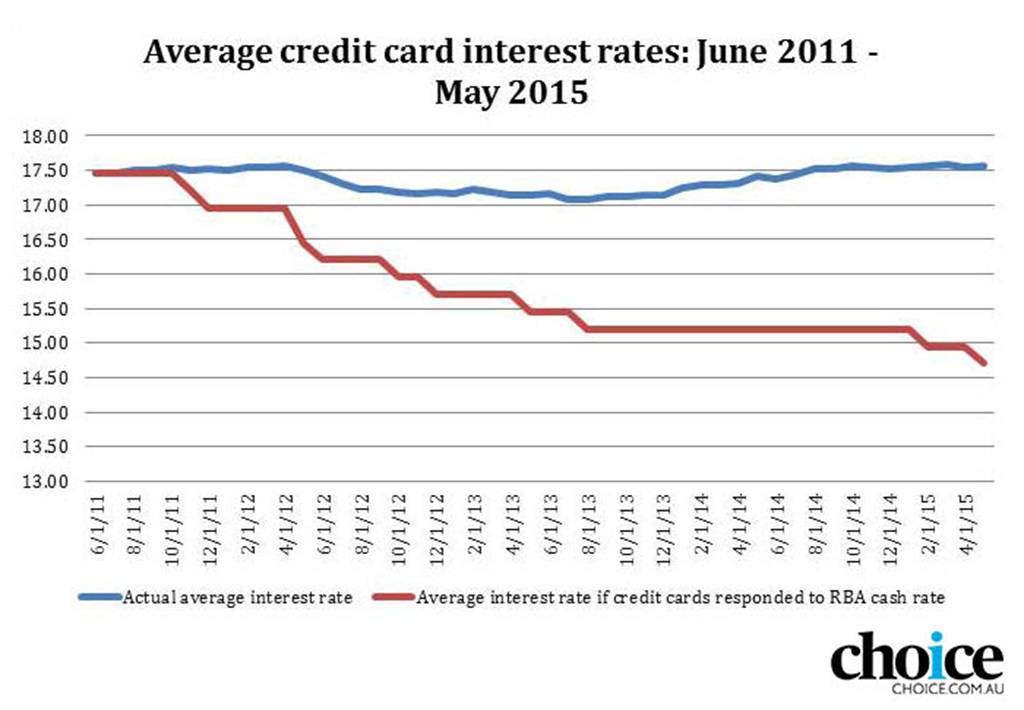

The research found fewer than one-fifth of the 55 major credit card providers between November 2011 and May 2015 adjusted their interest rates following an official interest rate cut.

The official cash rate is at a record-low of 2 per cent. The gap between the Reserve Bank's rate and credit card interest rates is at its widest since records began in 1990.

But in the past few years, interest rates for just about every other type of debt have plunged, baffling economists and consumers.

The top brass of Treasury and the Reserve Bank were interrogated about the record gap by Labor senator Sam Dastyari in June. They conceded it was a "good question" and they would take a closer look.

The Treasury has essentially advised Treasurer Joe Hockey there is no systemic problem in this part of the banking market. It also does not think the issue is a symptom of a lack of competition.

A Senate

committee will soon begin investigating into why Australia's big four branks are

charging such high rates without clear reason. Choice

will present more detailed findings of its analysis.

"We know the average credit card interest rate in June 2011 was 17.41 per cent, but instead of falling in-line with the cash rate it rose by 0.2 per cent over the last four years to 17.61 per cent by the 31st of May (2015) this year," said Mozo's Kirsty Lamont.

"We have also seen the average credit card annual fee rise from $94 in late 2011 to $115 in May 2015. Clearly consumers are getting a raw deal."

Steven Münchenberg, chief executive of the Australian Bankers' Association, insisted the banking industry was competitive, pointing to the vast array of credit card products on offer by at least 67 financial institutions.

"The interest rate on bank credit card products covers a broad range - from a low of 5.30 per cent to a high of 20.99 per cent. Each credit card product offers a range of benefits - from no frills to premium options," he said.

"Interest on credit cards is higher than it is for mortgages and some personal loans. This is because credit card lending is unsecured and therefore riskier. Banks need to factor in the risk that the person holding the credit card may default," he said.

"The interest rate will also reflect the various features of the credit card. It is these considerations that drive credit card interest rates, not the Reserve Bank's cash rate."