The real story behind the credit card debt headlines - Crikey - GLENN DYER AND BERNARD KEANE - JUL 05, 2018

Contrary to media reports, Australians are not being crushed under the rising burden of credit card debt, we're just using our cards differently.

The media love a financial distress story, as demonstrated by the constant — and entirely contrived — claims of rising “mortgage stress”. The latest version isn’t about residential mortgages, but credit card debt — or “debt trap” as the Australian Securities and Investments Commission put it yesterday when releasing a new report.

According to ASIC, “18.5% of consumers are struggling with credit card debt … while credit cards offer flexibility, they can present a debt trap for more than one in six consumers. In June 2017 there were almost 550,000 people in arrears, an additional 930,000 with persistent debt and an additional 435,000 people repeatedly repaying small amounts.”

Fairfax loved it, as did the ABC with headlines like “credit card users struggling under mountain of debt that may never be repaid”.

Credit card debt is a hardy perennial for the media, and newspapers have been writing about it since the first consumer credit card, Bankcard, arrived in wallets and purses in the mid-70s. And, sure, there are a lot of dodgy deals in credit cards, slack issuers, usurious interest rates and poor regulation. But yet more Credit card debt trap! headlines obscure the changing nature of credit card usage, which is a far more interesting story that has recently been explored by the Reserve Bank. Its April 2018 Financial Stability Review carried this important observation “the changes in the use of personal credit and in borrower type confound the usefulness of personal credit indicators as measures of overall household financial health.”

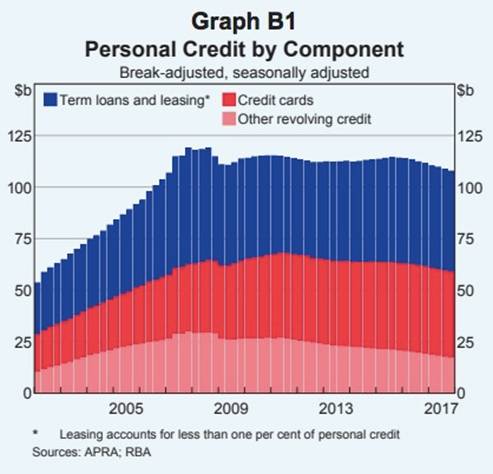

Those of of us with the financial capacity now use credit cards differently. “The share of credit card debt accruing interest has declined from 72% in 2007 to about 62% currently,” the RBA found. “The growing habit of repaying it in full each month accounts for the stable stock of credit card debt, despite their increased use as a means of payment.” That is, we’re using credit cards more like debit cards, or for large purchases we don’t need to borrow for.

But some users lack the financial resources to avoid credit card interest: the RBA suggests “it is younger and lower-income borrowers [who typically rent] who constitute a larger share of those using credit cards to fund purchases that are paid off gradually over time. Data from HILDA (Household, Income and Labour Dynamics in Australia Survey) also suggest renters are more likely to pay interest on credit cards than owner-occupiers, consistent with owner-occupiers having access to other sources of debt, and tending to be older and having higher income.” The bank also found HILDA data that suggested the proportion of credit card and motor vehicle debt held by renters had increased significantly in the thirteen years to 2016.

Plainly it’s inevitable that lower-income earners are more likely to struggle with debt, but the real story with credit cards is that it’s among renters and low-income earners that there is a growing problem; if anything, more people on higher incomes have learnt to avoid the usurious interest rates charged by banks.

The bank also noted something that the “household debt” panic merchants might not like: our overall level of personal debt (credit cards, personal loans etc) is falling. “After rising strongly in the years prior to the global financial crisis, personal credit balances from Australian banks have remained fairly stable for the past decade, at around $110 billion. This contrasts with the growth in mortgage lending, which has more than doubled during that period, so that the share of personal credit in Australian banks’ lending to the household sector has fallen, from 12% in 2009 to just 6% of late.”

Not exactly headline fodder, is it.