What happens if interest rates don't go up soon? The inflation 'genie' will be out of the bottle - ABCNews - David Taylor 22 March 2022

The economy is performing well, on paper at least.

Australian economic policy is getting rather awkward. Let me explain.

The economy is performing well, on paper at least. There's just one problem: a key policy lever is acting like the economy is in intensive care.

The Reserve Bank's cash rate target sits at 0.1 per cent — the lowest on record.

It's been at that rate since the height of the pandemic to help turbocharge the economy.

So, should it be higher? Well, that's where it gets awkward.

Why is the cash rate target so low?

The interest rate that variable-rate borrowers pay for their loan is set, in part, by the cash rate.

It's what the Reserve Bank charges the banks to borrow in the short term or overnight.

The RBA doesn't set the cash rate, it instead determines the cash rate "target".

That means it literally goes into the money market and signals to traders where it wants the "cash rate" to be and the market, normally, dutifully follows.

The system works so well that significant shifts in the cash rate target have materially influenced the level of short-term interest rates more broadly and what the banks have felt comfortable charging for their variable interest rates (benchmarked on short-term money market rates).

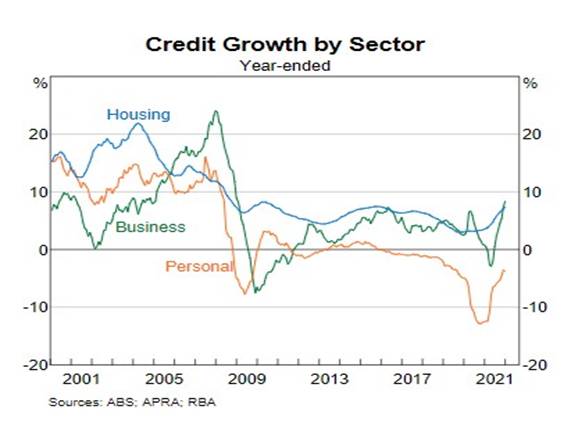

Credit growth by sector. (Source: ABS, APRA, RBA)

It's therefore crucial that as lending or credit growth slows or falls, the Reserve Bank can influence the cash rate to increase borrowing again.

Lending fell dramatically during the guts of the pandemic, which is why the cash rate target fell to 0.1 per cent. But should it still be that low?

Reasons for a higher cash rate target

The Reserve Bank governor Philip Lowe recently said it was "plausible" the bank could raise the cash rate target later this year.

This slight change in messaging is because the economic landscape has changed.

Underlying inflation is sitting within the RBA's target bank — basically where it wants it to be — but headline inflation is sitting uncomfortably high at 3.5 per cent.

The unemployment rate is at multi-decade lows, while gross domestic product is at a tidy 3.4 per cent.

In other words, evidence is emerging that the economy is growing, and it's generating jobs and inflation.

But is that what's going on in reality?

Space to play or pause, M to mute, left and right arrows to seek, up and down arrows for volume.

Two types of inflation

Inflation comes in two forms: demand-pull and cost-push.

Demand-pull inflation is generated by workers with higher pay having the confidence to spend up big at the shops.

Cost-push inflation comes from business bosses passing on the higher costs of production to customers in the form of higher prices.

Cost-push inflation is now deeply embedded. But is demand-pull inflation a thing?

You could argue it is because shoppers have been spending, but as the latest gross domestic product figures show, households have been dipping into their savings in order to fund it.

The increase in consumer demand in the economy doesn't stem from confident workers spending their extra cash from a pay rise.

Inflation expectations

Do you feel it starting to get a bit awkward?

The RBA senses the need to raise interest rates because inflation is showing signs of getting hot, but at the same time it's not seen as the kind of inflation that's likely to hang around or become more intense.

That said, if businesses are worried their costs will climb higher still, they're more likely to compete or bid with other firms for inventory and supplies now, further adding to cost-push inflation.

Of course, higher interest rates won't necessarily aid this situation. It may actually make it worse.

That's because costs for businesses will remain high and they're likely to receive less revenue as consumers pull back on their spending to cater for higher borrowing costs.

The inflation 'genie'

It's enough to make you blush.

Inflation is rising. We all know this. It costs more to go out and about, and it seems to be getting worse.

Economists describe this sense of uncontrolled rising inflation as the inflation "genie" escaping from the bottle.

That is, whether it's cost-push or demand-pull inflation, once it starts creeping higher, getting it back under control, or back in the bottle, is challenging.

The RBA needs to anticipate an inflation break-out.(ABC News: Daniel Irvine)

The main policy tool to control inflation is the Reserve Bank's cash rate target, but you can't just raise the cash rate target and expect prices will fall. It doesn't work like that.

This part of the "interest rate policy cycle" is an art more than a science.

The RBA needs to anticipate an inflation break-out.

Up to now, the board has made the judgement that a break-out is unlikely because economy-wide pay rises, which lead to demand-pull inflation, appear some way off.

Where does this leave us?

Let's be honest. There's no way to make this analysis neat and tidy. It's awkward and messy.

Inflation is rising and there doesn't appear to be any indication it's coming back down.

ANZ Bank research shows, if anything, inflation expectations will push inflation up to 5 per cent or more.

The silver bullet is higher pay because that would make the higher cost of living more manageable, but that still seems like a pipedream.

Should the Reserve Bank start lifting interest rates?

The Russia-Ukraine war is creating a new supply shock and inflation will rise in response. What should interest rates do? Read more

The RBA is holding fire on interest rates because there's a danger tighter policy will derail a fragile economic recovery. But as economist Angela Jackson explains, you then run the risk of causing greater financial pain for households down the track.

"The main risk of the RBA holding fire for too long is higher inflation, which ultimately will require lifting interest rates faster and a greater risk of an economic slowdown," she says.

"There is also a risk of underpinning further increases in asset prices, which have grown massively in the two years since record low interest rates were introduced.

"This has increased wealth inequality and increases the risk of financial instability if those asset prices should fall significantly once interest rates inevitably start rising again.

"The slower the RBA can ultimately move on interest rates, the better to manage these risks."